The US-China fallout just opened a door, and these Indian companies are walking through it

")

China's loss is turning into India's opportunity—meet the 5 Indian companies riding the wave of global supply chain realignment.

As global giants rewire their supply chains, India is stepping into the spotlight.

With the US-China trade war redrawing the map of global manufacturing, multinationals are urgently scouting for alternatives to China—and India is emerging as a strong contender.

From a booming skilled workforce to government-backed incentives, the country is fast positioning itself as a manufacturing powerhouse.

For investors, this seismic shift opens up a unique window of opportunity.

In this article, we explore five Indian stocks poised to ride the wave of this geopolitical shake-up—companies that not only symbolise India’s rising economic clout but also offer serious potential for outsized returns.

Whether you're a market veteran or new to investing, these are the stocks you'll want on your radar in 2025.

Let’s dive in.

Aarti Industries

Aarti Industries Ltd, the flagship company of the Aarti group, is engaged in manufacturing organic and inorganic chemicals.

The company operates major manufacturing facilities across Gujarat—in Vapi, Jhagadia, Dahej, and Kutch—as well as in Tarapur, Maharashtra. It holds a strong market leadership in the NCB-based specialty chemicals segment.

The company manufactures speciality chemicals in benzene based derivatives. Key value chains include nitro chloro benzenes (NCBs), di-chloro benzenes (DCBs), phenylenediamines (PDAs), nitro toluene value chain, and equivalent sulphuric acid (ESA) & downstream.

Aarti Industries has 16 manufacturing units, 2 R&D centres, 5 co-gen power plants, over 100 products, over 700 domestic customers, and over 400 export customers in 60 countries with a major presence in the US, Europe, and Japan.

Geographically, the company generates 52% of its revenue from exports, with the remaining 48% coming from the domestic market. It also manufactures active pharmaceutical ingredients (APIs) at its facilities in Tarapur and Dombivli in Maharashtra, as well as in Vapi, Gujarat.

Coming to the financials, Aarti Industries reported a 15.4% growth in revenue in 9MFY25 and Ebitda growth came in at 5.8%. Ebitda margins however deteriorated from 15.1% in 9MFY24 to 13.8% in 9MFY25.

Aarti Industries is grappling with stiff competition and margin pressures in the near term. Its strategic focus on product innovation, long-term contracts, and joint ventures will be crucial to sustaining growth.

The company’s future performance will hinge on its ability to navigate these headwinds, control costs, and drive volume growth.

Shares of Aarti Industries have declined 49% over the past year, weighed down by muted financial performance and intense competitive pressures.

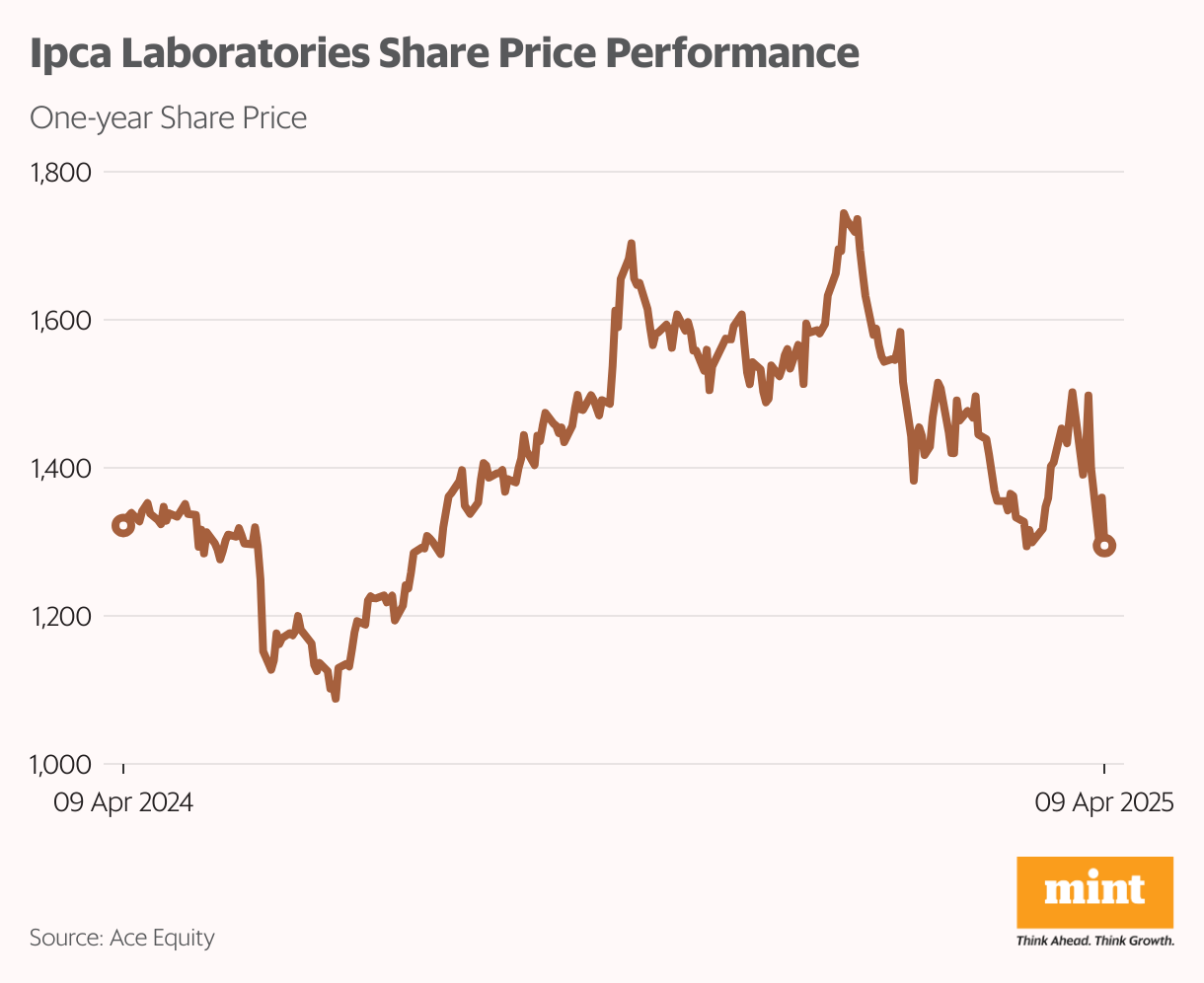

Ipca Laboratories

Ipca Laboratories is a fully integrated pharmaceutical company engaged in the manufacturing and marketing of over 350 formulations and 80 active pharmaceutical ingredients (APIs) across various therapeutic segments.

Ranked among India’s top 20 pharma firms, the company has built a strong global presence.

Ipca exports nearly 79% of its APIs and intermediates, supplying to over 100 countries, and is one of India’s leading API exporters. Its 18 manufacturing facilities across India cater to both domestic and international markets, producing APIs and formulations for pain, rheumatology, antimalarial, and haircare therapies.

Geographically, Ipca derives 46% of its revenue from India, followed by 18% from the US, 15% from Europe, 7% from Africa, 6% from Asia (excluding India), 4% from Australia, and the remaining 4% from other regions.

Around 70% of its revenue comes from the highly competitive pain management, cardiovascular, anti-diabetic, and anti-malarial segments.

On the financial front, the company reported an 18% year-on-year revenue growth for the first nine months of FY25, driven by broad-based performance across segments. Ebitda rose 29.8%, with margins improving from 17.6% in 9MFY24 to 19.4% in 9MFY25.

Looking ahead, management remains optimistic about sustained growth, especially in the chronic care and pain management categories.

Shares of Ipca Laboratories have remained largely flat, down 2% over the past year, supported by improving operational performance and promising future prospects.

Bharat Forge

Bharat Forge, a flagship company of the $3 billion Kalyani Group, is a leading manufacturer of forged and machined components for the automotive and industrial sectors.

It holds the distinction of being India’s largest exporter of auto components and ranks among the world’s top manufacturers of powertrain and chassis components.

The company generates 85% of its revenue from its core forgings business, producing critical components such as steel forgings, crankshafts, front axle assemblies, road wheels, and transmission parts. The remaining 15% comes from its growing defence vertical, which includes artillery systems, armoured vehicles, ammunition, and air defence solutions.

Bharat Forge has a strong global footprint, with 76% of its revenue coming from exports and just 24% from the domestic market. Its manufacturing base spans 15 locations across India, Germany, Sweden, France, and North America, with a total capacity of 0.65 million tonnes per annum (mtpa) for steel forgings, 52,000 mtpa for aluminium castings, and 77,700 mtpa for iron castings.

On the financial front, Bharat Forge reported a 2.2% year-on-year revenue decline for the first nine months of FY25, while profit after tax dropped 6.8%. However, operational efficiency improved, with Ebitda margins rising to 17.9% from 16.6% in the same period last year.

Also read: Bharat Forge on the edge as India-US trade pact holds the key to tariff relief

Looking ahead, the management remains upbeat about the company’s long-term prospects, buoyed by a robust order book in the defence segment and early signs of recovery in the domestic and North American commercial vehicle markets.

Despite recent business headwinds, which led to a 16% decline in the stock price over the past year, Bharat Forge’s global presence, product diversification, and strategic bets on defence position it well for a strong rebound.

Gokaldas Exports

Gokaldas Exports Ltd (GEX) is a leading player in the apparel export industry, engaged in the design, manufacturing, and sale of garments across men’s, women’s, and children’s categories.

With a strong client base that includes some of the world’s most prestigious fashion brands and retailers, the company exports to over 50 countries globally.

Backed by a workforce of over 54,000 employees—75% of whom are women—GEX has established a robust presence with manufacturing facilities in India, Kenya, and Ethiopia, and marketing offices in the UAE and the US. It operates over 30 manufacturing units worldwide, boasting a production capacity of 87 million pieces annually.

The company’s operations are powered by 30,000+ state-of-the-art machines, along with in-house capabilities like 3D design studios, certified testing labs, quilting and polyfill units, modern printing setups, and integrated embroidery systems.

GEX generates 83% of its revenue from exports, with the top three clients contributing about 50% to its standalone revenue. The remaining 17% comes from the domestic market.

Also read: Rupee unshaken amid US-China trade war. India may even gain from it.

On the financial front, the company reported a sharp 81.9% growth in net revenue for the first nine months of FY25, largely driven by recent acquisitions. Standalone revenue rose 19% amid an improving demand environment.

However, operating profit grew by a relatively modest 46.5%, as Ebitda margins narrowed from 10.8% in 9MFY24 to 8.7% in 9MFY25—reflecting pressure from acquisitions that are yet to operate at peak efficiency.

Looking forward, the management has guided for a 10–15% annual growth trajectory over the next 2–3 years, with a sharp focus on boosting margins alongside revenue expansion. The company is also targeting a milestone revenue of $1 billion in the coming years.

Despite a 3% dip in share price over the past year, GEX’s strategic global footprint, growing scale, and recovery in global demand position it well for long-term growth.

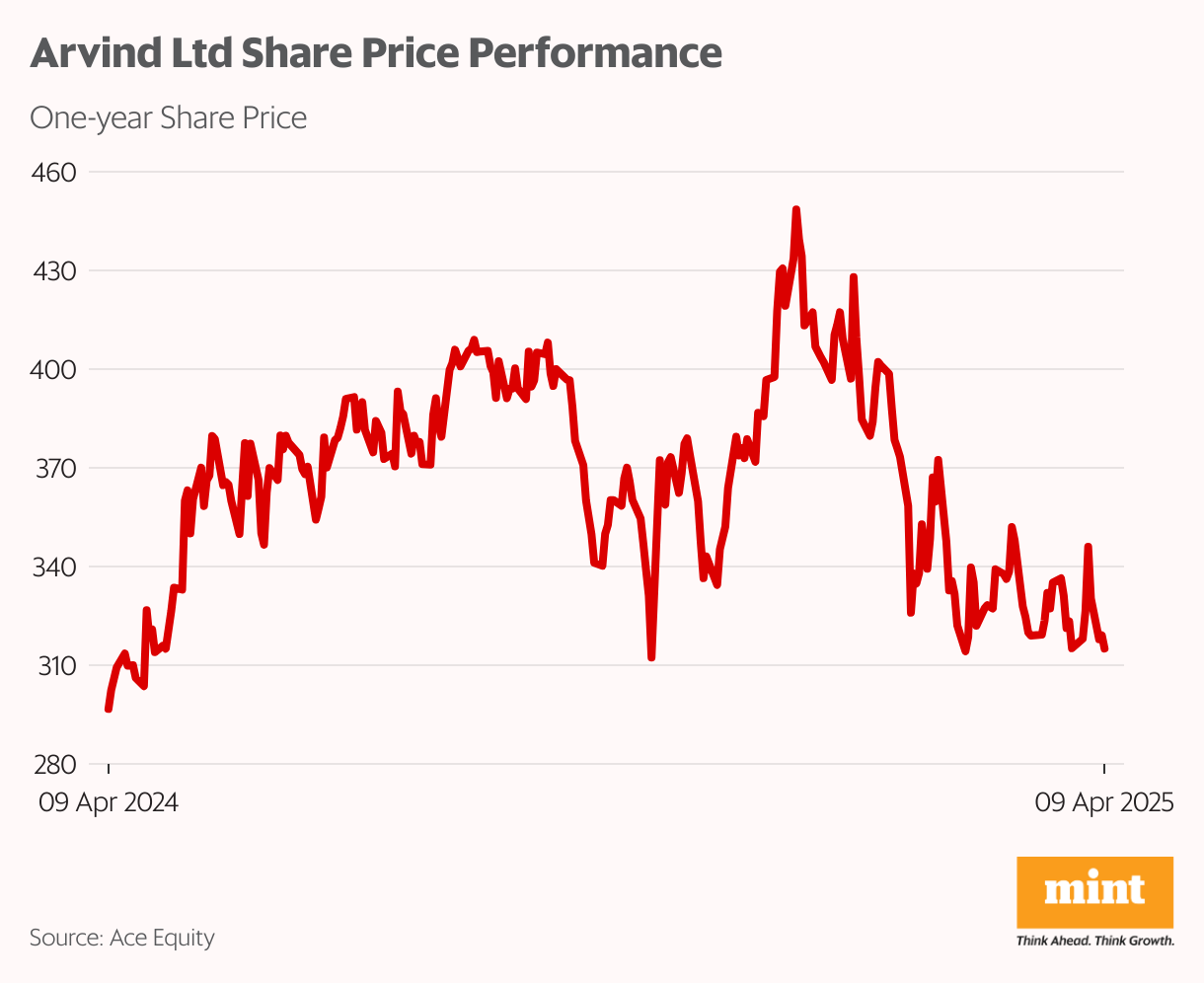

Arvind

Arvind Limited is one of India’s most established and vertically integrated textile companies, with a legacy spanning nearly eight decades.

The company is globally recognised as one of the largest manufacturers of denim and also produces an extensive range of fabrics, including cotton shirting, knits, bottom weights (khakis), and ready-made garments like jeans and shirts.

In addition to fashion textiles, Arvind has also made a strong foray into technical textiles with applications across diverse sectors such as human protection, filtration, conveyor belting, automotive, and construction.

With fully integrated operations across the textile value chain—from spinning cotton yarn to finished garments—Arvind enjoys significant operational agility, enabling it to adapt quickly to market demands and drive efficiency across its product lines.

The company derives 46% of its revenues from woven fabrics, 27% from garments, 19% from denims and balance 8% from other sources.

Arvind earns 49% of its revenues from India while the remaining 51% of revenues come from its key export markets of the US, UK, and EU.

The company owns and operates 9 manufacturing facilities located in Gujarat, Karnataka, and Maharashtra.

Coming to the financials, Arvind reported revenue growth of 7.9% while the operating profits were up by 1% for 9MFY25. Ebitda margins also deteriorated from 10.6% in 9MFY24 to 9.9% in 9MFY25.

Going ahead, the management expressed optimism about exports, with a focus on the US and Oceania markets, despite current uncertainties in Europe. The company also says that cotton prices remain a concern due to high MSPs and import duties, affecting competitiveness.

Arvind stock is up 6% in the last one year on the back of muted financial performance.

The road ahead

The US-China trade war, though disruptive globally, has opened a strategic window for India to emerge as a key node in global supply chains. As multinationals rethink their manufacturing footprints, Indian companies—from chemicals and pharmaceuticals to textiles and engineering—are well-placed to seize the moment.

While near-term challenges persist, strong fundamentals, export-oriented models, and strategic foresight position these firms as potential long-term winners in a shifting geopolitical landscape.

That said, investors must stay alert to rising market volatility and the risk of a broader economic downturn driven by continued trade retaliation.

With a disciplined approach, close tracking of global developments, and sound research, these companies could prove to be valuable additions to your portfolio.

Happy investing!

Also read: India’s gold demand stalls as prices spike, futures trade at discount amid volatility

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com