The week in charts: Reliance job cuts, Bangladesh crisis, US recession fears

- News and developments from the week gone by, through numbers and charts.

Every Friday, Plain Facts publishes a compilation of data-based insights, complete with easy-to-read charts, to help you delve deeper into the stories reported by Mint in the week gone by.

Reliance Industries Ltd reduced its workforce by 11% in FY24, while the Reserve Bank of India (RBI) is worried about the credit-deposit mismatch at banks. Meanwhile, recession fears in the US spooked markets around the world.

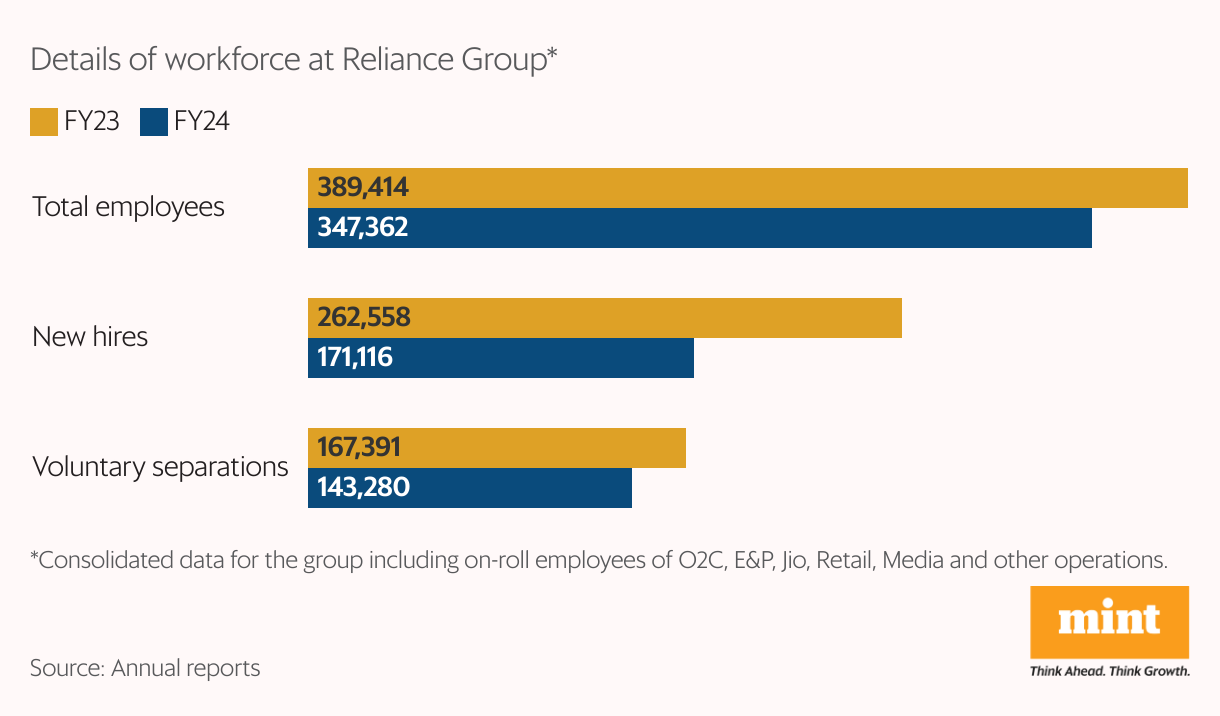

Reliance’s workforce reduction

The number of employees at Mukesh Ambani-led Reliance Industries Ltd fell by 42,052 to 347,362 in FY24 as the company has been keeping close tabs on its employee numbers, Mint reported. According to the company’s annual report, the biggest decline was in Reliance Retail, which saw its headcount fall by 38,029. However, overall voluntary separations (resignations) were lower in FY24 than in FY23. The conglomerate hired 171,116 new employees across businesses during FY24, 35% less than in the previous year.

RBI’s credit-deposit worry

The sharp rise in credit coupled with tepid growth in deposits have created a mismatch in funding, forcing banks to look for alternative, non-deposit sources of funds. RBI Governor Shaktikanta Das has expressed concern about the trend, saying the banks' recourse to short-term non-retail deposits and other instruments to meet the increasing demand for credit may expose the banking system to structural liquidity issues. He suggested that banks instead focus on mobilising household financial savings through innovative products.

US recession fears grow

25%: That's the probability of the US slipping into recession next year, according to Goldman Sachs. The investment bank increased its estimate from 15% after jobs data showed unemployment rates hit a near three-year high of 4.3%. Fear of a US recession spooked markets worldwide amid questions about whether the Federal Reserve has been behind the curve on slashing interest rates. Meanwhile, a rare interest rate by the Bank of Japan caused the unwinding of the yen carry trade, further roiling markets.

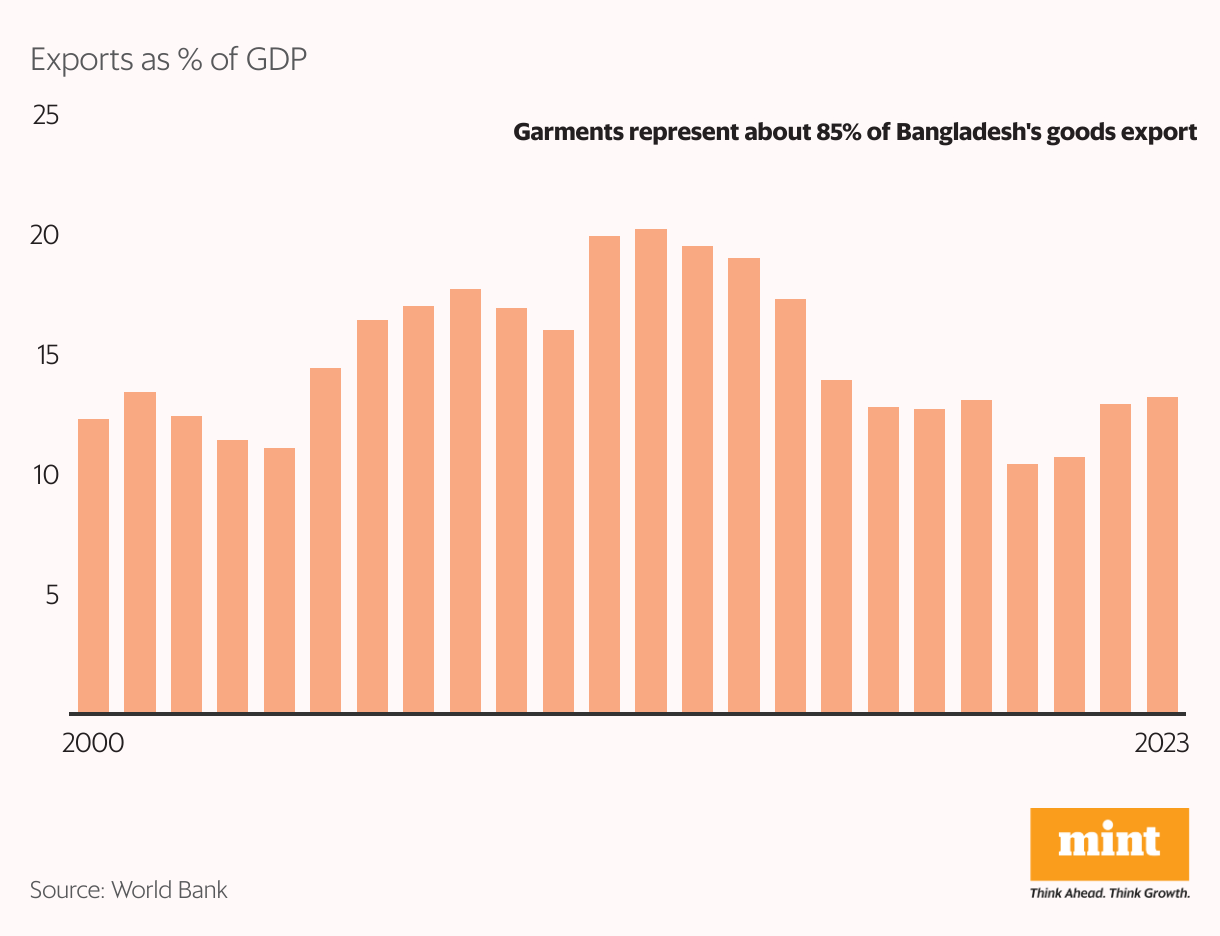

Bangladesh descends into chaos

Bangladesh slipped into crisis earlier this week after Prime Minister Sheikh Hasina was forced to resign and flee the country following months of protests against quotas in government jobs. The country had scripted a remarkable economic turnaround through exports, particularly of ready-made garments, overtaking neighbours India and Pakistan on per-capita income. However, the country started seeing the limitations of this export-led growth, with its share in gross domestic product (GDP) declining in recent years, a Mint analysis showed.

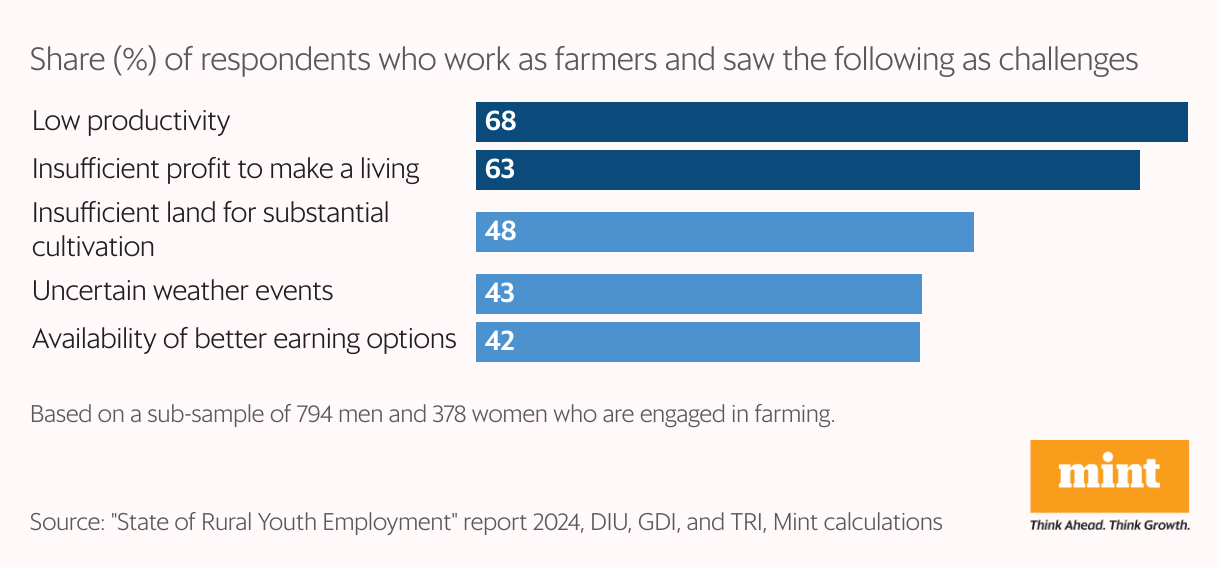

Most young farmers want out

Agriculture remains the biggest employer in rural areas, but an overwhelming majority of young people engaged in farming want salaried jobs instead, according to a new survey by Development Intelligence Unit (DIU), Global Development Incubator (GDI) and Transforming Rural India (TRI). More than 60% of the 1,172 respondents (young people engaged in farming) said they wanted to leave agriculture because of low productivity and insufficient profits. Limited access to markets and debt traps for small farmers were other factors.

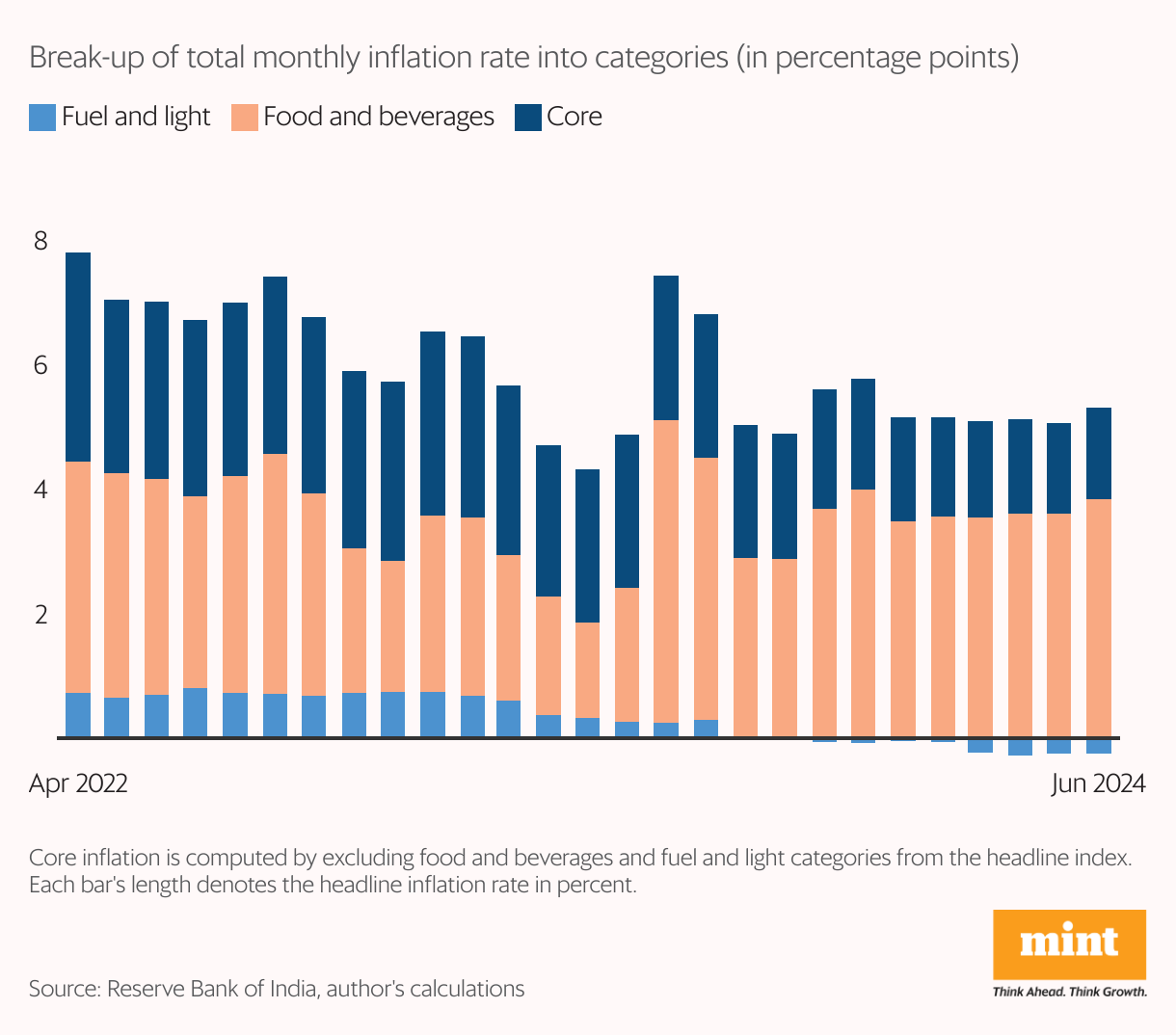

Food inflation can't be wished away

The Economic Survey 2024, tabled last month, proposed excluding food inflation from the overall inflation target. A Mint analysis showed that this may not be a practical idea. Large and persistent food price shocks significantly affect non-food prices, and household inflation expectations are closely aligned with what plays out in the food basket. High food prices therefore cannot be wished away. The solution lies in a flexible, situation-driven approach to managing inflation, like the one RBI is currently practising.

More medical seats after exam fiasco

3,000: That's the number of additional undergraduate medical seats planned by the union government in the wake of criticism it received over the recent medical entrance exam fiasco. This would will take the total number seats to 115,000, Mint reported. The National Medical Commission approved the setting up of 28 private medical colleges to increase the seat count.

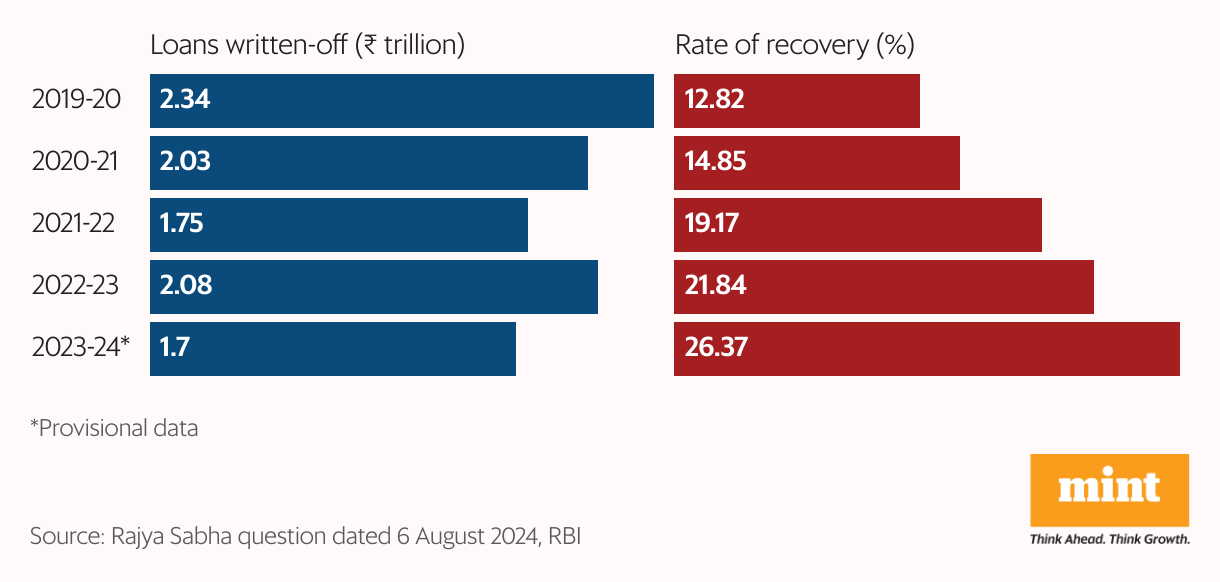

Chart of the week: Recovering bad loans

Indian banks have managed to recover barely a fifth of bad loans over the past five years, data shared by the government in the Rajya Sabha showed. The average recovery rate stood at 19% between FY20 and FY24, during which time ₹9.9 trillion worth of loans were written off. However, the recovery rate has increased over the years, from 12.8% in FY20 to 26.4% in FY24.

Follow our data stories on the“In Charts" and“Plain Facts" pages on the Mint website.