Why we should not write off the e-rupee yet

")

Despite the initial push for central bank digital currencies by many nations, the adoption of CBDCs has been slow across the globe, including that of India’s e-rupee. However, the future holds better prospects.

In 2019, Meta announced plans to launch a private digital currency. Fearing an onslaught of private cryptocurrencies, some countries responded by announcing their own central bank digital currencies (CBDC). Fast forward to today: Every G20 nation is exploring a CBDC, with 13 countries having plans in the pilot stage. Yet CBDCs have barely made a dent in national payment systems.

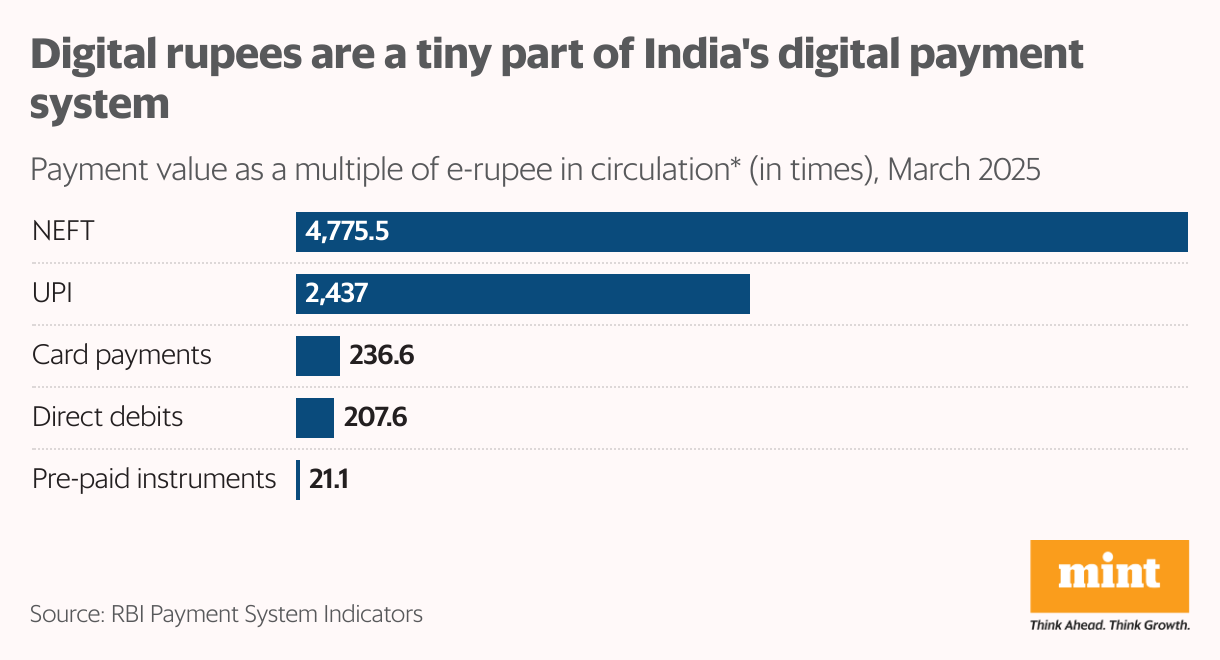

India launched the e-rupee for individuals in December 2022. And yet, at the end of March 2025, the value of the e-rupee in circulation, at ₹1,016 crore, was a tiny drop in the ocean of India’s digital payment ecosystem.

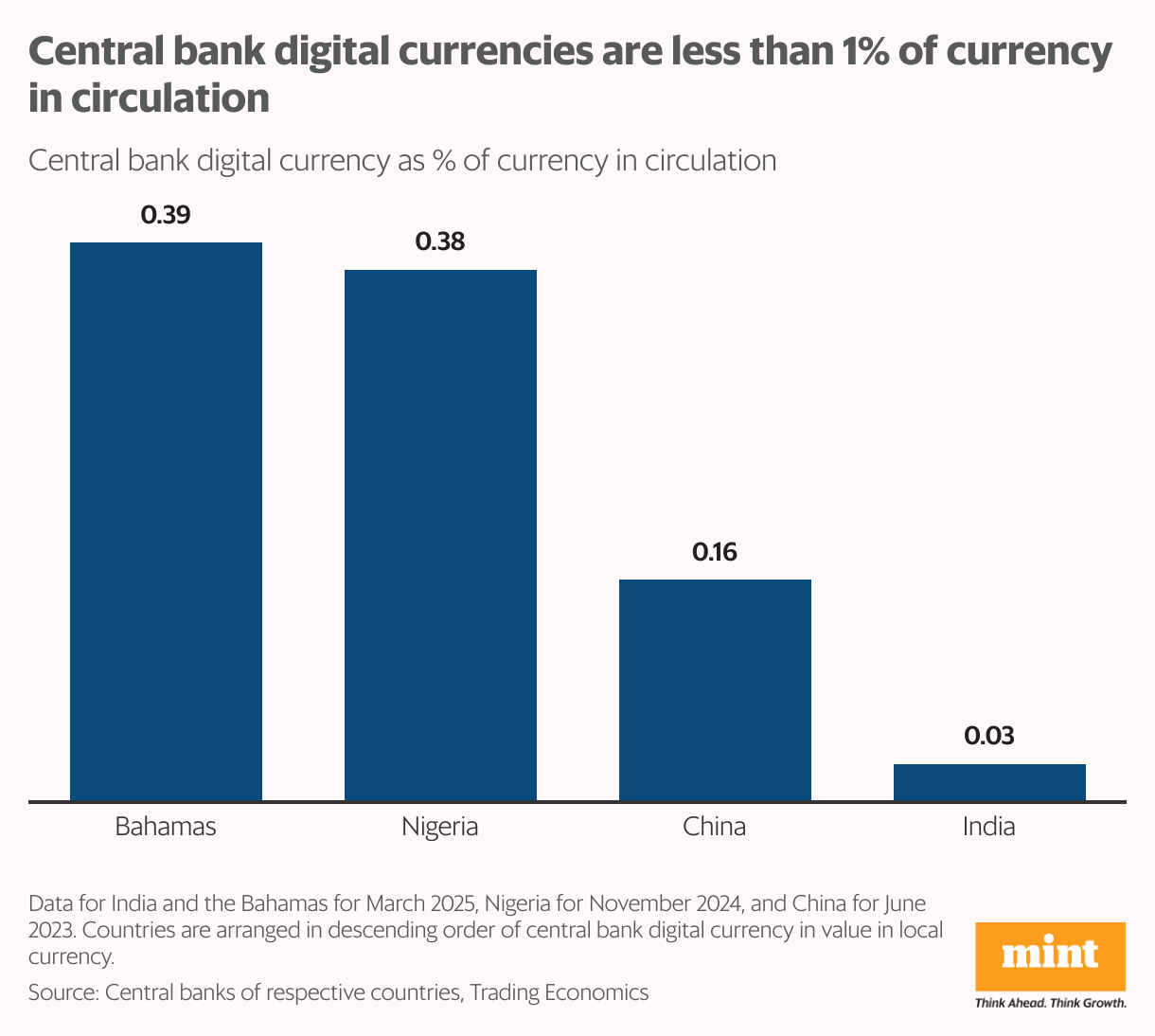

The slow uptake of the digital rupee mirrors the experience of other countries. CBDCs launched earlier (Nigeria, China) and in countries with higher financial inclusion (Bahamas) also show low adoption rates.

Nigeria launched the e-naira in October 2021; by May 2024, there were only 13 million e-naira wallets, many inactive (Nigeria’s population was 232 million, and it had over 200 million mobile phones in 2024). China’s e-CNY, launched in 2020, hit 180 million wallets by mid-2024, but reports suggest that many of the accounts are dormant.

The value of CBDCs currently in circulation indicates poor public demand and a lack of incentive to shift from existing payment methods. Yet it would be wrong to conclude that the CBDC experiment was a failure, or to dismiss the e-rupee. In the long run, the success of the e-rupee will depend on how it is rolled out and what use-cases it can cater to.

Patient rollout

The Reserve Bank of India has been in no rush to roll out the e-rupee. The digital rupee remains at the pilot stage, available only to some customers of participating banks and non-banks. By going slow, and testing use-cases patiently and systematically, RBI has minimized outages and execution problems that plagued CBDC pioneers like Nigeria.

Any effort to force adoption of the e-rupee could erode trust in the currency. Nigeria faced this situation in 2022 when old naira notes were withdrawn and replaced with new notes. Nigeria’s central bank claimed the note ban would create a more cashless society, but the resulting cash shortage caused much hardship and severely eroded people’s trust in the system. Worse, it did not have a lasting impact on the use of the digital naira.

India hasn’t even offered cash incentives to encourage adoption of the e-rupee. This is probably wise. Typically, consumers take advantage of such incentives and go back to old payment modes when the incentive ends. China gave “red packets" of CBDCs during the Lunar New Year in 2021 to incentivise digital wallet downloads, but there is no evidence that it translated to greater use of the e-CNY.

All that said, RBI’s two smartest moves related to the digital currency have been allowing two non-banks to offer e-rupee wallets and making digital rupee wallets compatible with the ubiquitous UPI. Non-banks have a different customer base from banks and tend to be innovative in their product design. And in a country where the majority of digital payments ride on UPI, it would have been impossible for any digital wallet to succeed without being integrated with it.

The e-rupee’s potential

There are two broad reasons to continue developing the e-rupee.

First, it is a geopolitical imperative.

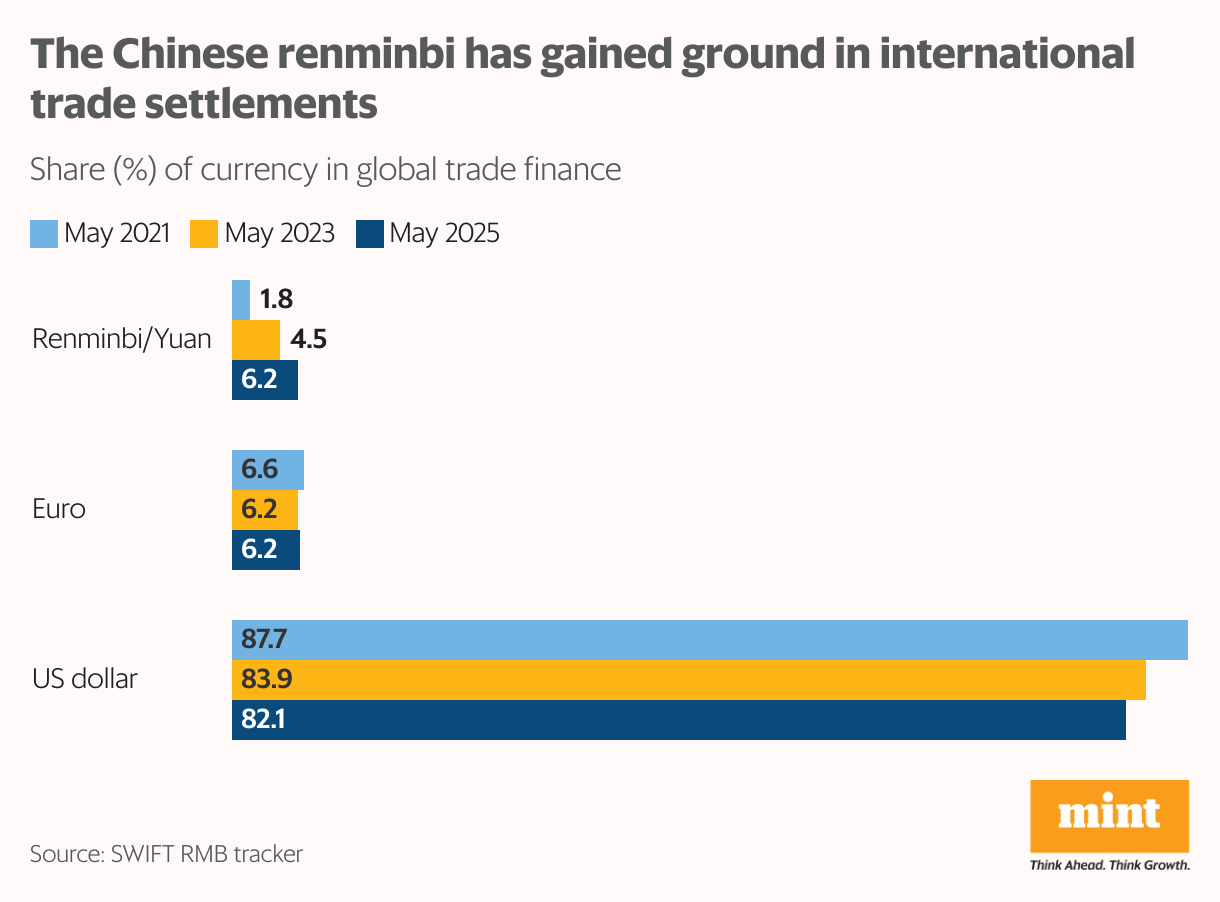

As China pushes to internationalize its currency, the share of renminbi in global trade financing has gone up significantly. China has already built fintech infrastructure to settle cross-border transactions that bypass the US-dominated Swift.

In response, several central banks are working on projects to link multiple CBDCs with the objective of facilitating fast and cheap international payments. Developing robust infrastructure will allow the e-rupee to link with other CBDCs when it becomes possible; this will be a big plus for India, given the size of the country’s inward remittances.

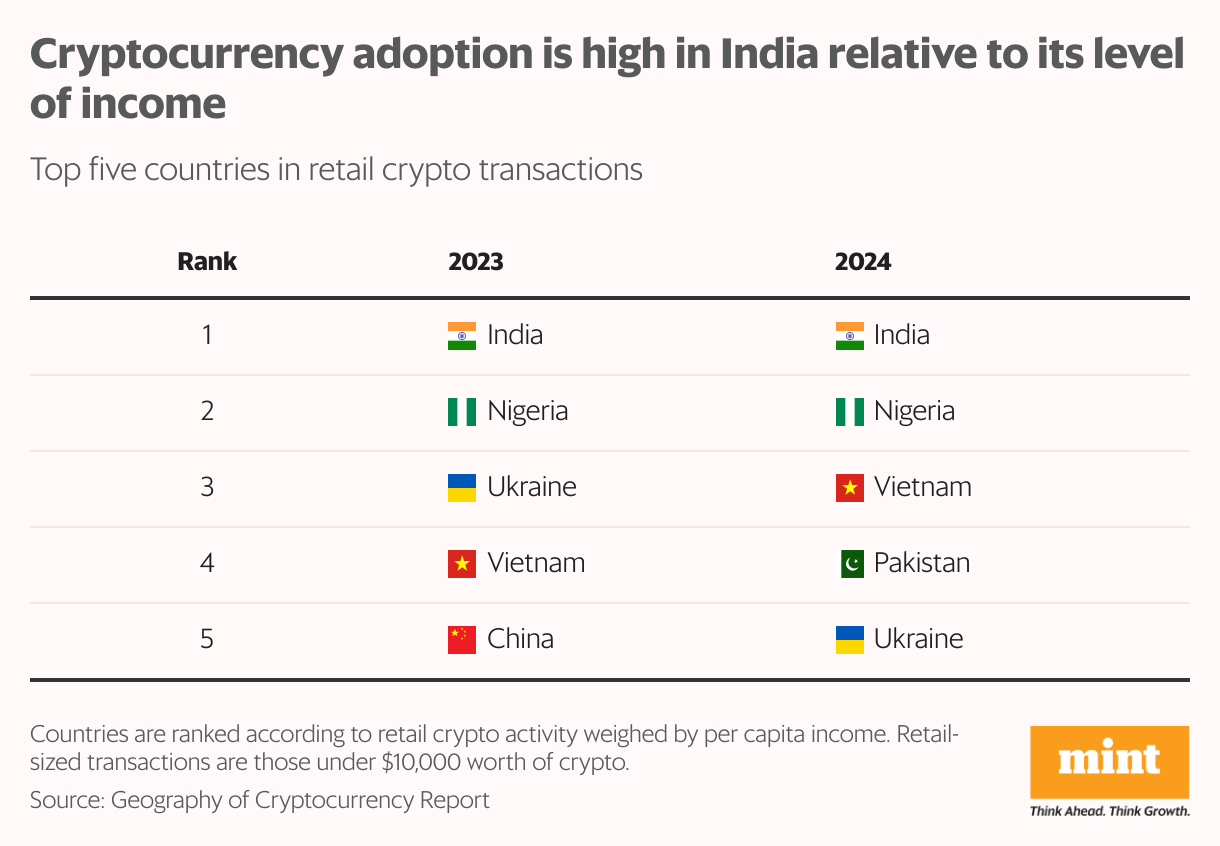

The rising popularity of cryptocurrencies in India could help drive greater adoption of the e-rupee. India’s crypto adoption is quite high relative to its income level, and the e-rupee can be an effective foil for cryptocurrencies: it runs on the same secure blockchain technology but offers a safer store of value.

Second, new use-cases for the e-rupee are continually being introduced and refined based on user experience. Direct transfer of government benefits to individual e-rupee wallets (as recently done in Odisha) is now par for the course.

The real excitement is in programmable e-rupee. Programmed agricultural loans to tenant farmers in Andhra and Odisha have been piloted—these ensure that credit is used only to buy farm inputs from approved vendors. HDFC Bank has introduced user-programmable e-rupee wallets, which let the user decide the location and validity of use.

RBI is also exploring offline usage, which can be a game-changer for remote rural areas. For example, e-rupee wallets can be pre-seeded in mobile phones in disaster-prone areas. Such wallets can be programmed to activate when disaster strikes, to give digital fund access to the affected population.

The author is an independent writer in economics and finance.