Opinion

Opinion

Time for India to revamp the Income Tax Act and ease compliance burdens

Summary

- New legislation could be designed to offer taxpayers as well as the tax administration relief. A leaner and simpler Act could also ensure that India gets its rightful share of tax revenues. Let’s revamp the 1961 law to support the Indian economy’s growth trajectory.

While presenting the Union Budget 2024 in July, Finance Minister Nirmala Sitharaman mentioned that the government would undertake a comprehensive review of the Income-tax Act,1961 (“the Act") to make it concise, lucid and easy to understand and thereby reduce disputes and litigation besides providing certainty to taxpayers.

The Act has had a long journey starting from 1961, spanning more than six decades and counting. Perhaps this is the longest surviving form of income taxation in India.

Income taxation during the pre-independence era started in 1860 when Sir James Wilson introduced the first Indian Budget, which proposed taxation of income. This Act was replaced by newer laws in 1886, 1912 and in 1961.

Also read: Direct Tax Vivad Se Vishwas scheme, 2024 to come to force from 1 October

Ever since its introduction in 1961, the Income tax Act has been bombarded with changes every year in order to stay current and cater to the growing needs of the economy, changes in business requirements, globalization and so on.

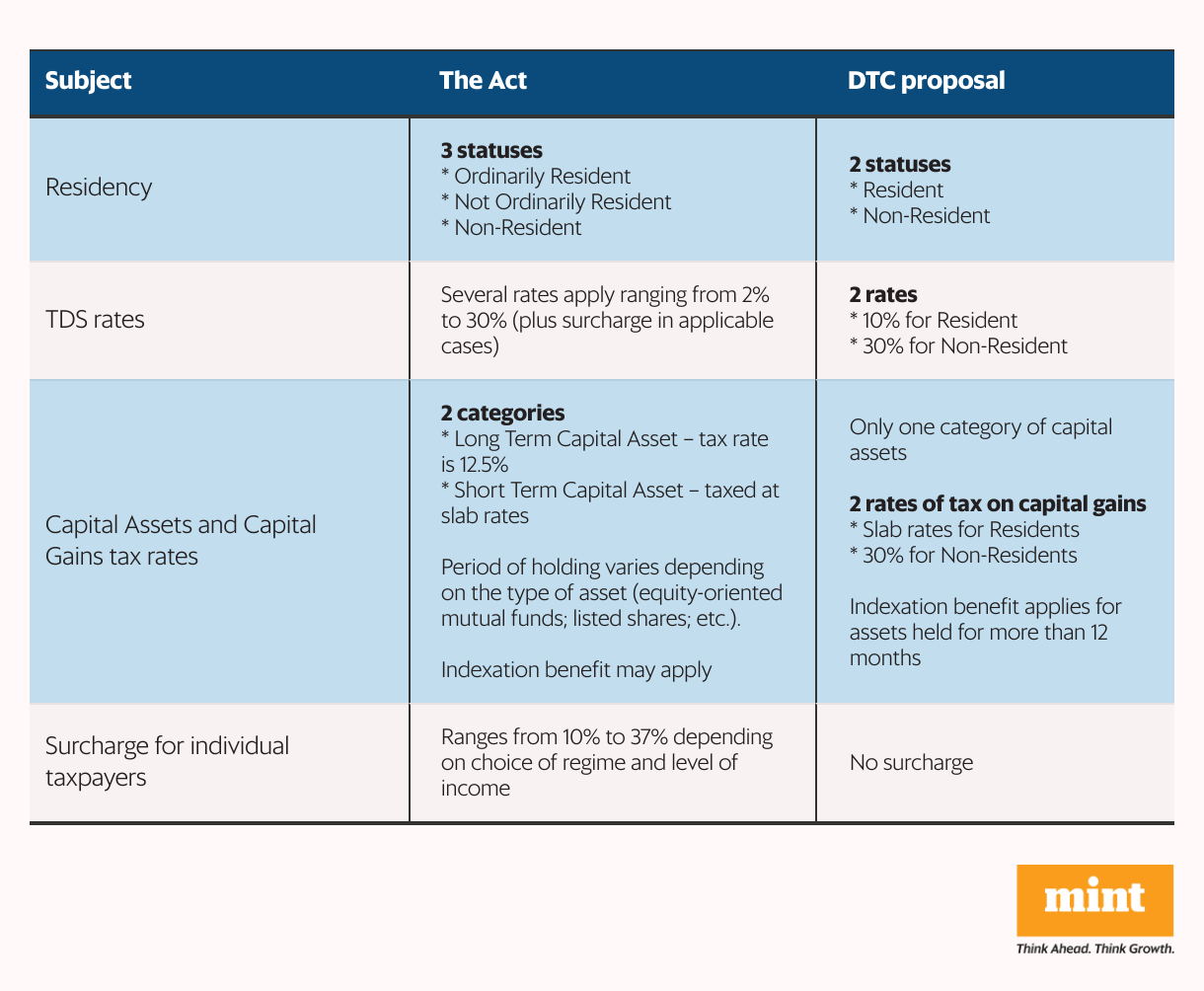

It is important to note that this is not the first attempt to revamp or simplify the income tax legislation. The government had introduced a draft of the Direct Tax Code (“DTC") in 2009 for public opinion, proposing a number of changes to simplify tax laws. Some of these changes are listed in the accompanying table, comparing them with the current provisions of the Act.

In 2017, the Government of India constituted a six-member committee to draft a new tax law to replace the existing Income Tax Act.

Further, consecutive budgets have been amending the Income Tax Act so as to facilitate easy compliance and simplify taxes. For example, the introduction of a simplified tax regime as an alternative to the regular tax regime (for taxpayers to choose between the two), is a way to ease compliance. Another example would be the rationalization in capital gains taxation brought in by the latest budget.

However, the fact remains that India’s tax legislation is old, even if some of its archaic provisions have been removed and replaced by newer ones. This practice not only keeps the Act updated, but also increases complexity with every such patch.

With increasing complexity comes increasing difficulty in interpreting the law’s provisions, giving rise to disputes and long drawn-out litigation. Despite increased monetary limits for appeals, disputes awaiting decisions by courts on interpretation of the law are on the rise.

Also read: Net direct tax collection grows 16% annually to ₹9.95 trillion up to 17 Sep

The government has taken measures to reduce litigation from time to time. The interim Budget of 2024 announced withdrawal of tax demands of ₹25,000 or less (prior to 2009-10) and ₹10,000 (2010-11 to 2014-15) or less. A mechanism to settle tax disputes, Vivad Se Vishwas (VSV), was offered in 2020 and again in 2024.

Tax authorities have taken advantage of technology in order to monitor compliance and the benefits of these have been availed by taxpayers. The ready availability of data on the tax portal and faster processing of refunds are examples.

Ease of compliance and ease of doing business are becoming crucial, considering that business is expanding across boundaries. The government has made significant efforts in reforming labour related legislation for wider coverage, better benefits and easier administration.

A simple revamp of the Income Tax Act could offer much-needed relief to all sections of taxpayers as well as the tax administration. A leaner and simpler Act that’s suited to today’s technology-driven environment is the need of the hour.

This would also ensure that India gets its rightful share of tax revenues in proportion to the government’s involvement in the economy, and without eroding its base.

Also read: Can I revise my income tax return to claim certain DTAA benefits?

Tax legislation that caters to the evolving needs of the country and taxpayers in today’s ever changing business and technology environment would support the economy’s growth trajectory.

Sudhakar Sethuraman is partner, Deloitte India.