Prachi Mishra: The Indian economy is at a pivotal point

")

Evolving global conditions present India opportunities, domestic growth is showing momentum and inflation looks manageable, but policymakers must be careful in managing a few key challenges. Here’s why the next few quarters will be critical.

The economic landscape has shifted dramatically this year. What seemed like an inevitable march towards global recession has given way to cautious optimism, driven primarily by an unexpected de-escalation of trade hostilities between the world’s two largest economies.

US President Donald Trump’s decision to scale back tariffs—from an initial increase of 10 percentage points to a peak of 145 percentage points and then declining by 115 percentage points following the 12 May US-China trade deal—has fundamentally altered the global economic trajectory.

This trade détente couldn’t have come at a better time for India. As tariffs between the US and China decline, leaving residual increases of just 30 percentage points on US imports from China and 10 percentage points on Chinese imports from the US, global supply chains are beginning to recalibrate.

Also Read: Trump’s tariffs: Turfed out but raring to return

For India, this presents an unprecedented opportunity to position itself as a reliable alternative in global value chains, particularly as companies seek to diversify their manufacturing bases.

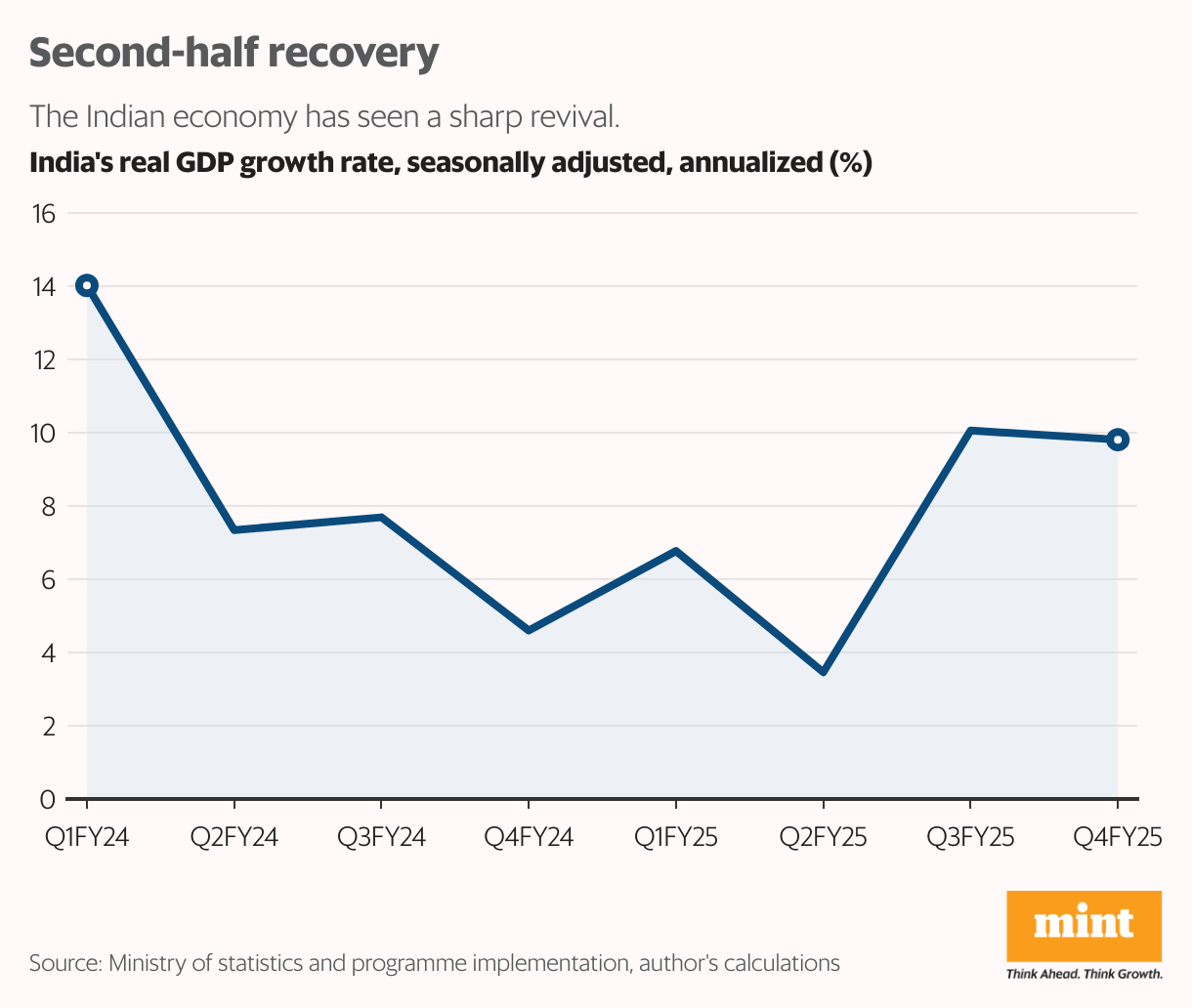

Beyond favourable global winds, India’s domestic economy is also showing signs of revival. The most recent gross domestic product (GDP) data reveals a robust and above-consensus 7.4% year-on-year growth and 9.8% seasonally adjusted annual rate in the first quarter of calendar year 2025—a figure that would have seemed optimistic just months ago. This isn’t merely a statistical quirk. High-frequency indicators across the board paint a picture of economic acceleration.

Industrial production, non-oil imports, vehicle registrations and air passenger traffic all point in the same direction: upward. Foreign institutional investors have returned as net buyers of Indian equities. The only cloud has been some temporary disruption due to airport closures from the border conflict, but overall, it has proven manageable.

Perhaps most encouragingly, inflation appears to be cooperating with this growth revival. Headline consumer-price inflation showed further moderation in April, while the momentum of core inflation, though rising in line with the economic recovery, remains well-contained. Declining crude oil prices can provide additional tailwinds if retail fuel prices were to adjust accordingly.

Also Read: RBI’s policy review: Why this time is truly different

This improving backdrop raises critical questions about the direction of monetary policy. The Reserve Bank of India has already delivered meaningful stimulus—50 basis points of policy rate cuts plus additional measures equivalent to roughly 100 basis points of easing through cash reserve ratio reductions and liquidity injections. The question is how much further to go and at what speed.

Economic theory suggests that as long as actual output remains below potential—creating a negative output gap—an accommodative policy will be appropriate, especially when fiscal space is limited. Current estimates suggest this output gap still exists, though it has narrowed significantly to roughly one-fourth of its previous magnitude relative to early this year. A comparison between the actual and potential real rates points to roughly 50 basis points of additional easing space, but the pace should be measured, given global uncertainties.

Also Read: Mint Quick Edit | Will inflation relief spell a stable rupee this year?

Encouragingly, money market conditions are finally showing signs of proper transmission, with call money rates now trading below the repo rate—exactly what monetary authorities want to see for effective policy propagation.

Yet, even as cyclical conditions improve, several structural issues may require attention. The rupee’s depreciation in the first quarter of 2025 (partly offset during the last two months due to dollar weakness)—2% against the dollar, 3% against trading partners and 5% in real effective terms—reflects reduced foreign exchange intervention amid declining inflation differentials.

While some depreciation may benefit competitiveness, policymakers must carefully assess whether the currency remains overvalued in this new global environment in which supply chain repositioning is creating opportunities for export-oriented economies.

More fundamentally, India faces a potential growth puzzle. Despite dramatic improvements in physical and digital infrastructure over the past decade, recent estimates suggest potential growth of only around 6%, well below the 7.5-8.0% range estimated a decade ago. Understanding and addressing this disconnect between infrastructure investment and productive capacity will be crucial for sustained long-term economic growth.

Also Read: India’s growth and urban planning: On different planets

India must also navigate evolving global financial realities. The recent US credit rating downgrade, while overdue given America’s debt trajectory, sends important signals about the fiscal sustainability of the US sovereign. It could also raise questions about whether we’re seeing early signs of a gradual erosion of the dollar’s ‘exorbitant privilege’—its unique ability to finance deficits without consequence. Even so, the dollar’s dominance as both a currency for transactions and a safe haven for savings is too deeply entrenched to dislodge.

For India, this underscores the importance of exploring opportunities to internationalize the rupee and of engaging with credit rating agencies. Research suggests these agencies place excessive weight on current debt stocks relative to future fiscal prospects, a bias that may not fully capture India’s improving economic fundamentals.

India stands at an inflection point. Global trade reconfiguration, domestic momentum and manageable inflation provide a rare confluence of favourable conditions. But success isn’t guaranteed. It will require careful monetary policy calibration, a focus on supply-side reforms and proactive engagement with global financial markets.

The next few quarters will be critical. If India can maintain this positive momentum while addressing structural challenges, it could emerge from this period significantly stronger and better positioned in the global economy. The foundations are in place; execution will determine whether this opportunity translates into sustained prosperity.

These are the author’s personal views.

The author is professor of economics at Ashoka University and head of Ashoka Isaac Centre for Public Policy.