PSU banks are winning the home loan race against private lenders. Here's why.

monitoring of small loans.")

Private sector banks faced significant challenges in FY25 due to more stress in unsecured loans, less liquidity, and stricter Reserve Bank of India monitoring of small loans.

MUMBAI : Public sector banks have been gaining market share over their private sector peers in mortgage or home loans, thanks to an aggressive push in tier-3 cities and beyond, and as private sector banks grapple with margins.

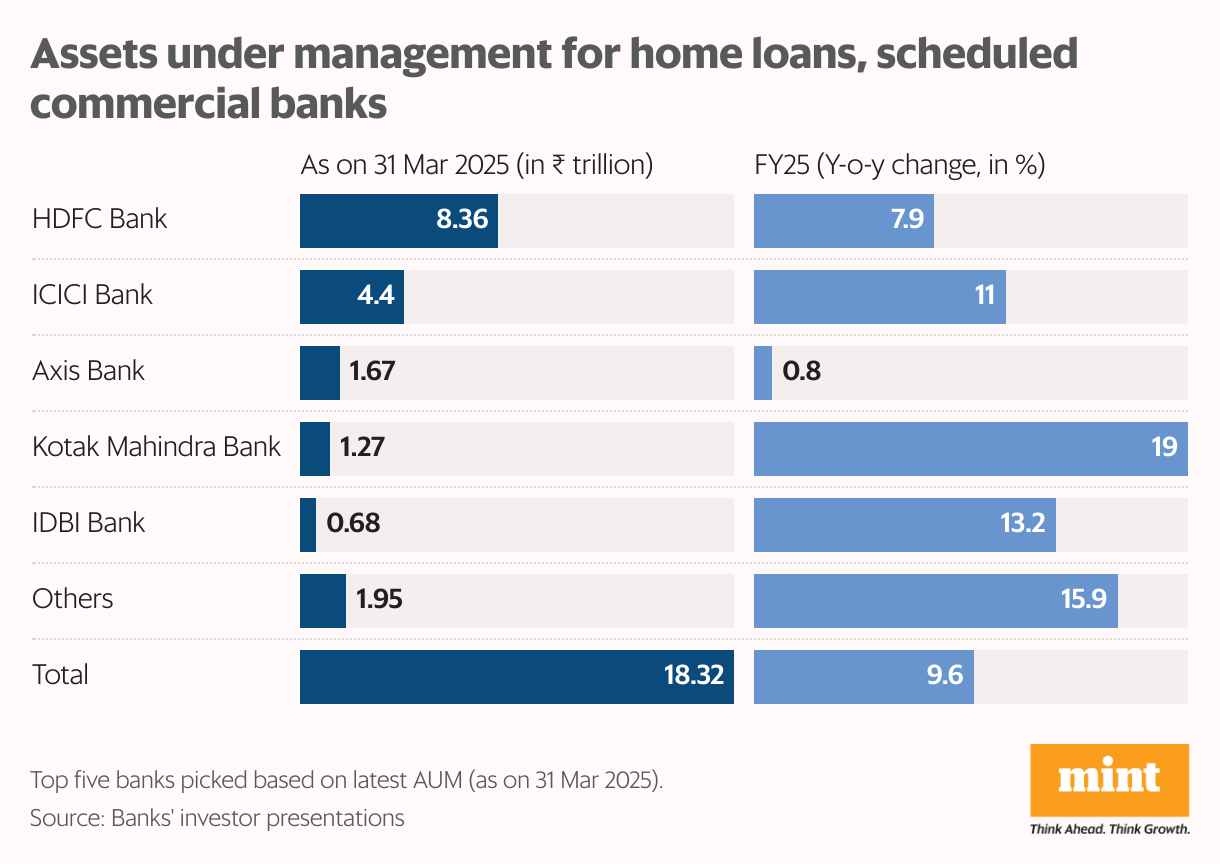

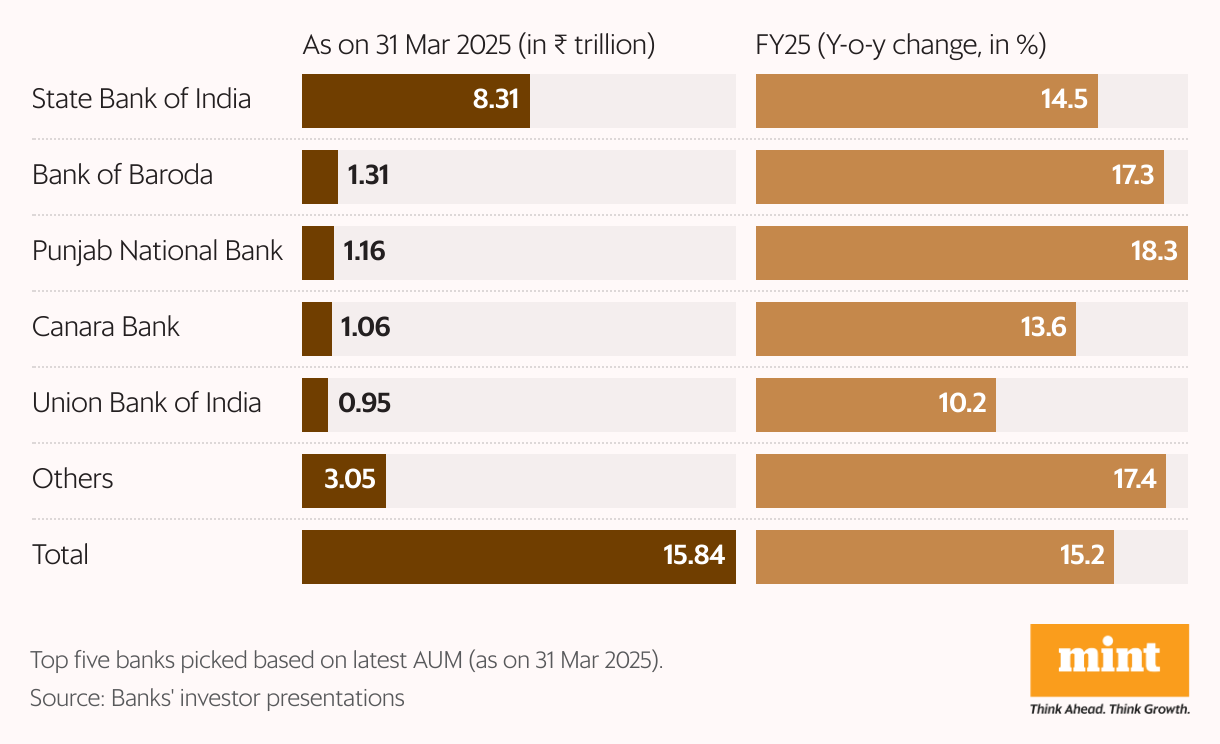

As of the end of FY25, the market share of PSU banks in home loans rose to 46.4% from 45.1% a year ago, whereas that of private banks fell to 53.6% from 54.9%, as per data compiled by Mint. The growth in PSU banks’ home loans portfolio outpaced that of private banks in FY24 as well.

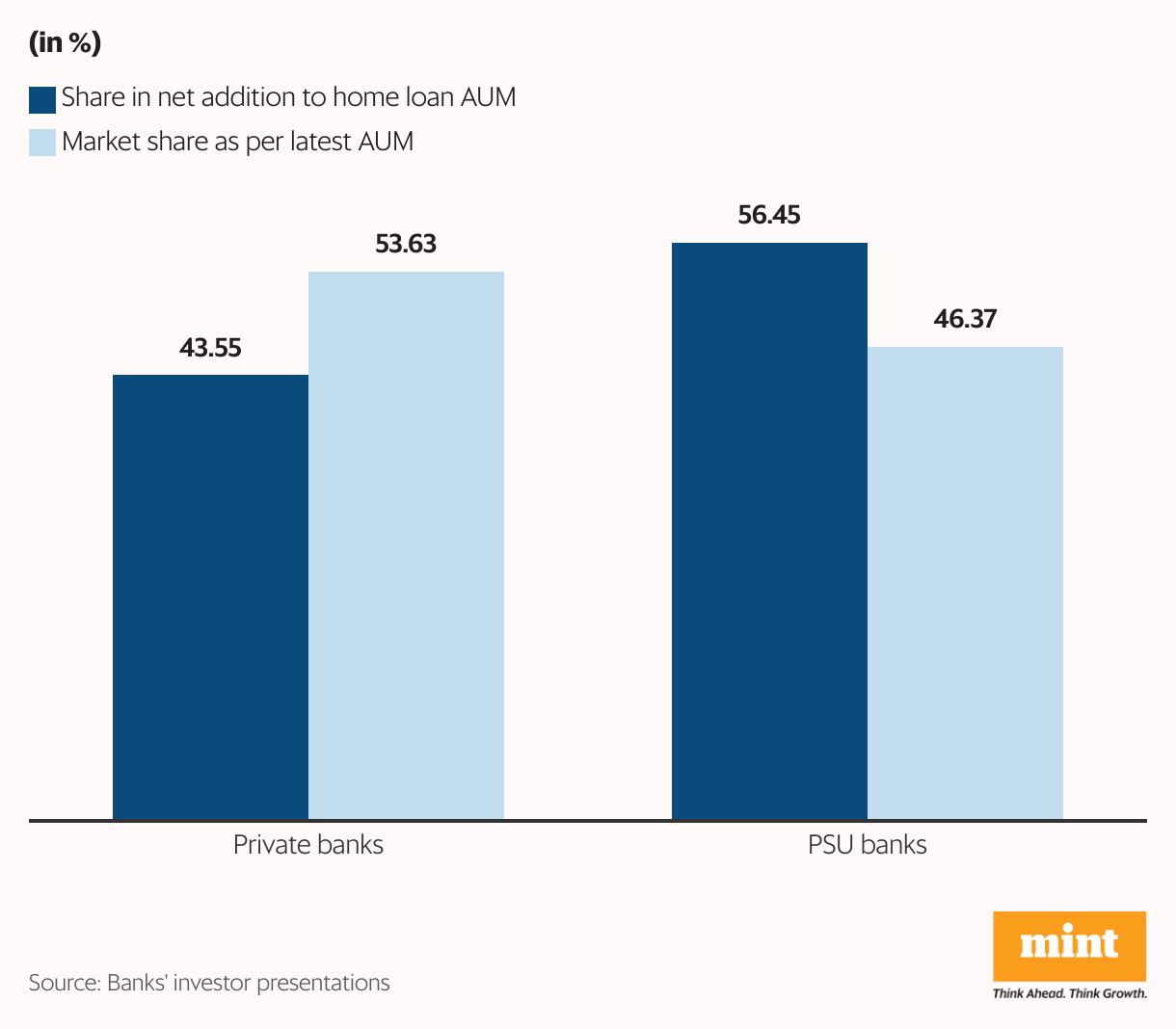

State-owned lenders added home loans worth ₹2.1 trillion to their balance sheets, amounting to a market share of 56.5% in terms of loans distributed in FY25. In comparison, private sector banks added home loans worth around ₹1.6 trillion, or 43.6% of the loans for the year.

Ankit Jain, associate director, India Ratings & Research, said the growth in home loans for PSU banks was due to the focus on retail loans.

Also Read: Bank, NBFC investments in AIFs may get smoother

“Because of subdued economic activity over FY25, PSU banks were largely focused on the retail segment, primarily mortgage and vehicle segments, which have historically displayed controlled delinquencies," Jain said.

What also helps is that home loans are safer and more profitable than lower-yielding corporate loans. Further, the private sector banks faced significant challenges in FY25 due to more stress in unsecured loans, less liquidity, and stricter Reserve Bank of India (RBI) monitoring of small loans, he added.

Tough times

“Till 3-6 months back, RBI had a hawkish view on monetary policy and as a result, the cost of funds were relatively higher and margins were under a bit of squeeze. As a consequence, banks, especially private ones, had challenges in lending very aggressively given that it’s a low-margin business," said Amit Diwan, chief distribution officer, India Mortgage Guarantee Corp. (IMGC). Compared to PSU banks, private ones also have more options and product lines to lend in, he added.

In a 31 March report, CareEdge Ratings had said that it expects the housing loan market, including banks and housing finance companies (HFCs), to grow at a CAGR of 15-16% over FY24-30.

Industry experts believe increased competition from PSU banks will persist in this segment as they look to grow their retail portfolios owing to the secured nature of home loans.

“If they’re happy being a low-margin business and want the share of retail assets to grow, the best way to do that is home loans. For most PSU banks, other than SBI, the retail assets are still a relatively smaller part of the balance sheet and so there is a conscious attempt to grow this book," said a senior official at a private sector bank, adding that home loans have the highest preference as they are considered the safest asset class.

Also Read: Lower capital requirements for bank loans to NBFCs to ease funding woes

On the other hand, private sector banks have been looking to protect their margins by slowing down growth in lower-yielding retail segments and lending more to unsecured and higher-yielding segments such as personal loans, credit cards and MSME loans.

The starkest slowdown in growth was for Axis Bank, which saw its home loan portfolio grow only 1% on year in FY25. In the bank’s Q4 FY25 earnings call, managing director and chief executive officer Amitabh Chaudhry said that, given the constraints on deposit mobilisation and growth in FY25, the bank chose to prioritise growth in certain asset classes and control growth in others.

PSUs working hard

“Assuming liquidity remains (and) flows sustain into the deposit side, we do believe that the platform is there for both growth and profitability. And as that deposit growth opens up, you will see growth start coming back across various asset classes," said Axis Bank's Chaudhry.

IMGC’s Diwan believes that what has helped PSU banks is that these lenders have put a lot of work into becoming competitive in distribution, digitisation and improving the loan turnaround time (TAT)—all of which is now bearing fruit.

Also Read: PNB Housing eyes affordable, emerging segments to boost loan yields

“PSU banks are making a proactive effort to reach out to channel partners and developers, and expand their own sales team. Further, there is buoyancy and demand in tier 2 and tier 3 and beyond cities, where PSU banks are better placed to cater to funding requirements given higher customer trust and their expansive branch network," he said.

Key takeaways

- PSU banks’ mortgage loan market share rose to 47.7% in FY25, while private sector banks saw a decline.

- Private sector banks struggled with higher stress in unsecured loans, tighter liquidity, and stricter RBI regulations.

- State-owned banks focused on mortgage and vehicle loans due to lower delinquency rates.

- To protect margins, private lenders shifted focus to higher-yielding segments like personal loans and credit cards.

- PSU banks improved distribution, digitization, and loan processing speed, boosting their presence in tier 2 and 3 cities.