No carrot, only stick: Why the RBI has gone beyond moral suasion and fines

- In recent times, the RBI has imposed several stringent measures against banks and NBFCs to ensure compliance. By targeting some of the largest names in the industry—HDFC Bank, Kotak Mahindra Bank, JM Financial, Bajaj Finance, IIFL Finance, Paytm Payments Bank—the RBI is setting a precedent.

Mumbai: The regulatory bomb exploded a little after 5:30 pm on 3 May, a Friday, and bankers were ill-prepared. In a draft guideline, the Reserve Bank of India (RBI) proposed stricter rules for financing of projects, especially those in the construction phase. The banking regulator wanted lenders to set aside up to 5% of such loans as provisions or buffers instead of the prevailing 0.4%. While the move left bankers flummoxed, analysts were quick to point out that lenders’ profitability would take a hit. Industry insiders, meanwhile, said that the proposal was simply plugging a gap in the RBI’s earlier guidelines, issued in 2019.

But banking experts believe the proposed rule will discourage lenders from financing projects, which could jeopardize private investment at a time when India’s private capex cycle is just picking up. At the very least, they say, there will be an increase in lending rates to infrastructure projects, as banks will pass on the cost of higher provisioning.

A private banker, who deals in corporate loans, speculated that the norms might have been put in place because of developments in two of the most talked about sectors, renewables and roads, which have seen several little-known and small companies bidding for projects. The regulator may have been concerned that the next wave of bad loans would originate from these sectors if banks were not careful, said the banker, who sought anonymity in order to speak freely. “It came as a surprise, but I think the RBI has its reasons; it has an ear to the ground,” he added.

The stricter project financing rule is just one of several stringent measures that the RBI has proposed and imposed in recent times as it seeks to tighten norms, eliminate loopholes and ensure total compliance by the entities it oversees.

In essaying its role, the regulator has not shied away from taking on big corporate-backed financial services entities, irrespective of who is at the helm. Take the case of Kotak Mahindra Bank, founded by billionaire banker Uday Kotak, which was pulled up in a strongly-worded circular recently. On 24 April, the RBI barred the bank from onboarding new customers through its online portal and mobile app, and restricted it from issuing fresh credit cards after it found “serious deficiencies” in the bank’s information technology (IT) system. In a regulatory filing, the bank said it has taken concrete steps to adopt new technologies to strengthen its IT systems.

Last October, it had barred Bank of Baroda from onboarding new customers on its bob World app in the wake of media reports about fake onboarding. That ban was lifted this month. In the past, it had barred HDFC Bank from issuing fresh credit cards over glitches in its system and American Express from doing the same for failing to comply with its data storage norms.

The number of cases where banks and non-banking financial companies (NBFC) have faced the regulator’s ire has increased over the past year. Other lenders that have been subjected to regulatory clampdowns of late include JM Financial, Bajaj Finance (now revoked), IIFL Finance and Paytm Payments Bank. Several others have been fined for not following its guidelines.

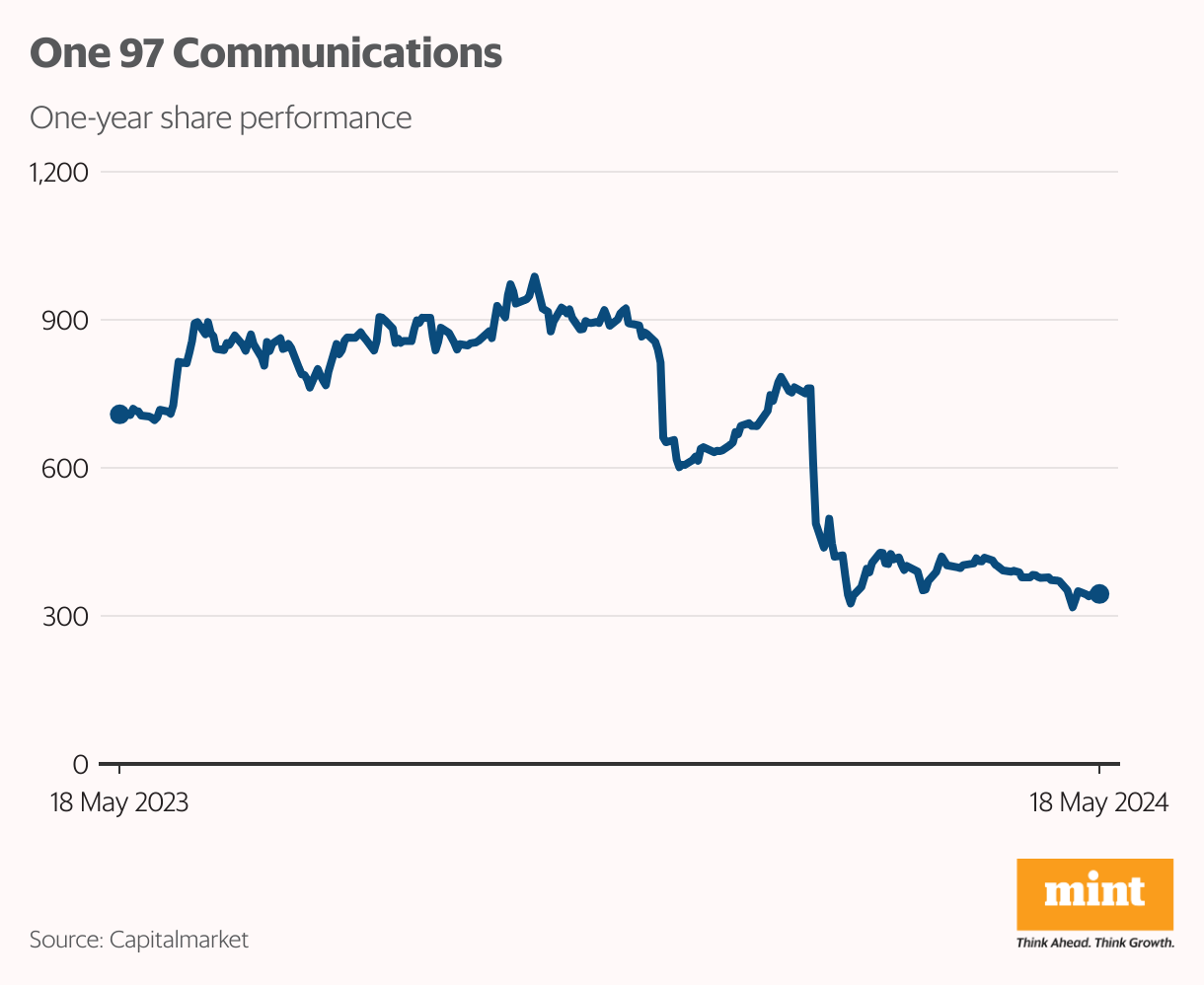

In the case of Paytm Payments Bank, on 31 January, the eve of the Union Budget, the regulator barred any addition of funds to accounts, wallets and Fastags (electronic toll collection system) after 15 March, effectively choking an important source of revenue. Shares of the bank’s parent, One 97 Communications, plunged 20% on Budget Day. One97 Communications told the stock exchanges it expects RBI’s action to have a worst-case impact of ₹300-500 crore on its annual earnings before interest, taxes, depreciation, and amortization (Ebitda), going forward.

“By targeting some of the largest names in the industry, the RBI is setting a precedent that size does not grant immunity, promoting a culture of compliance across all financial entities,” said Vatsal Gaur, partner, King Stubb and Kasiva, advocates and attorneys.

If former RBI governor Raghuram Rajan’s tenure was characterised by a clean-up of bank balance sheets, the extended term of Shaktikanta Das appears to be focused on establishing better governance standards through business restrictions rather than merely relying on paltry penalties.

“During Rajan’s time, the focus was on the credit quality of banks and strengthening their balance sheets, as well as focusing on getting credit to the weaker sections. Today, we have a reasonably strong financial system and with the evolution of the India tech stack, the thrust now is to ensure that this growth is data-driven, and by people who understand risk,” said Vinit Mehta, managing director of Motilal Oswal Private Equity.

It isn’t just banks and NBFCs. Although fintechs do not officially fall under its purview, the RBI has not hesitated to rein them in when they enter its domain, especially those that are in the business of lending. With the goal of protecting consumers, the regulator stepped in to check the explosion of new-age startups issuing loans to customers, especially after numerous reports of loan app scams by Chinese syndicates, usurious interest rates and strongarm tactics by collection agents. While many of those were fly-by-night operators, other fintechs that did not have a lending license were sourcing loans for banks and NBFCs for a fee. Many fintechs applied for an NBFC license in order to extend loans off their own books. Only three of them—Cred, Jupiter and BharatPe—have been approved, according to reports.

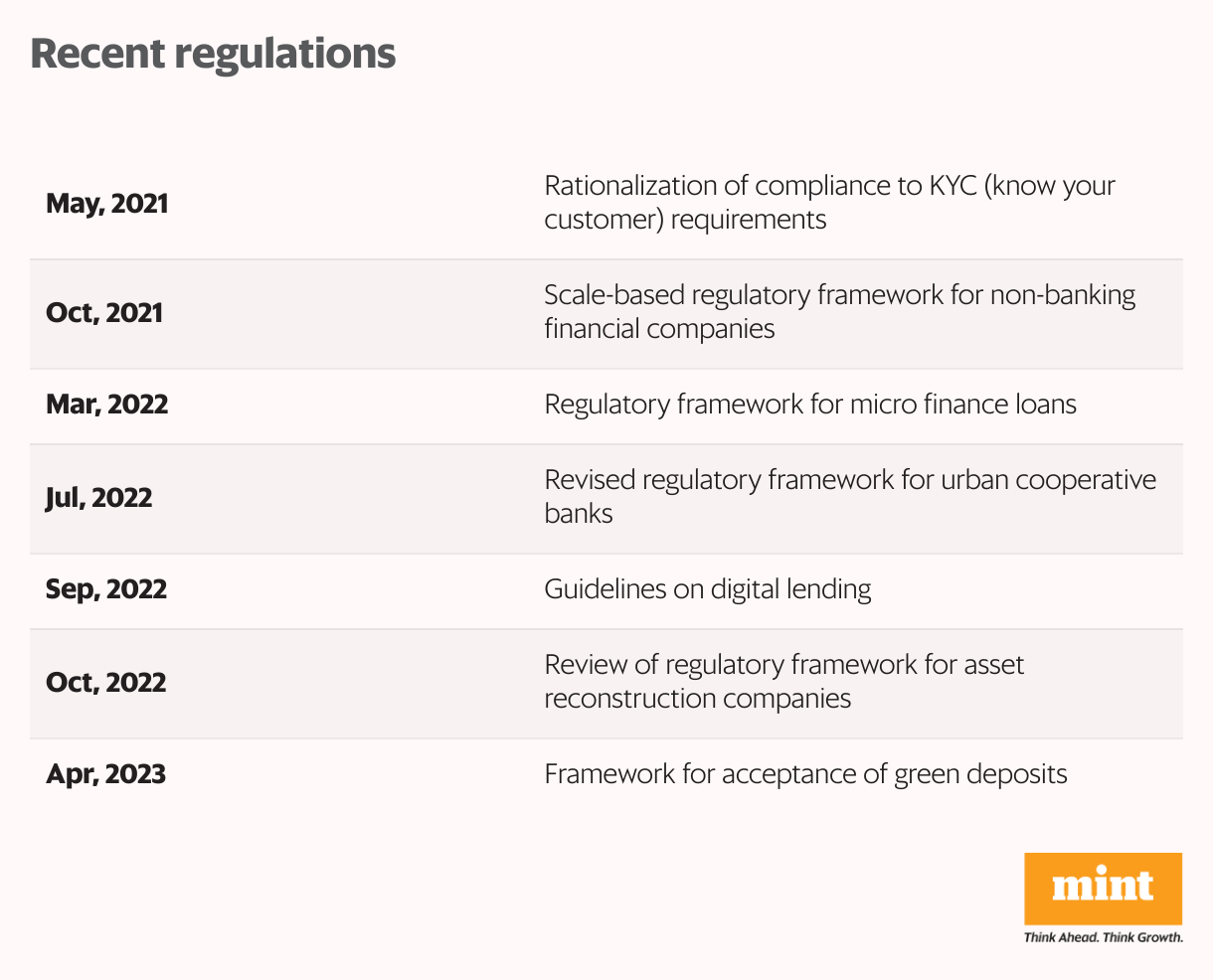

In September 2022, the central bank issued guidelines to regulate digital lending in India, including guidelines for collection of fees by lending apps, reporting of all digital loans to credit bureaus, and usage of customer data. In 2020, it had pushed fintechs acting as payments intermediaries to apply for a Payments Aggregator license, forcing them to start over.

Simply put, under Das, who was appointed in December 2018 and whose second term will end this December, the 90-year-old institution has taken it upon itself to crack down on governance issues and get lenders to colour within the lines, even if this miffs the market.

And the market certainly is miffed. The project financing proposal, for instance, elicited an anguished reaction from Suresh Ganapathy, managing director and head of financial services research at Macquarie Capital. “The sector now is left, right and centre seeing regulatory risks and actions…While every objective of the regulator is to strengthen the balance sheet of banks and make counter cyclical buffers when the health of the sector is the best seen in the last decade or so…what is surprising is how draconian these rules are,” he wrote in a mail to clients three days after the RBI proposal.

NBFCs on Edge

While many in the industry acknowledge that there are issues the regulator needs to address, they say that too often, the RBI does not give companies enough time to react, especially when it comes to NBFCs and fintechs.

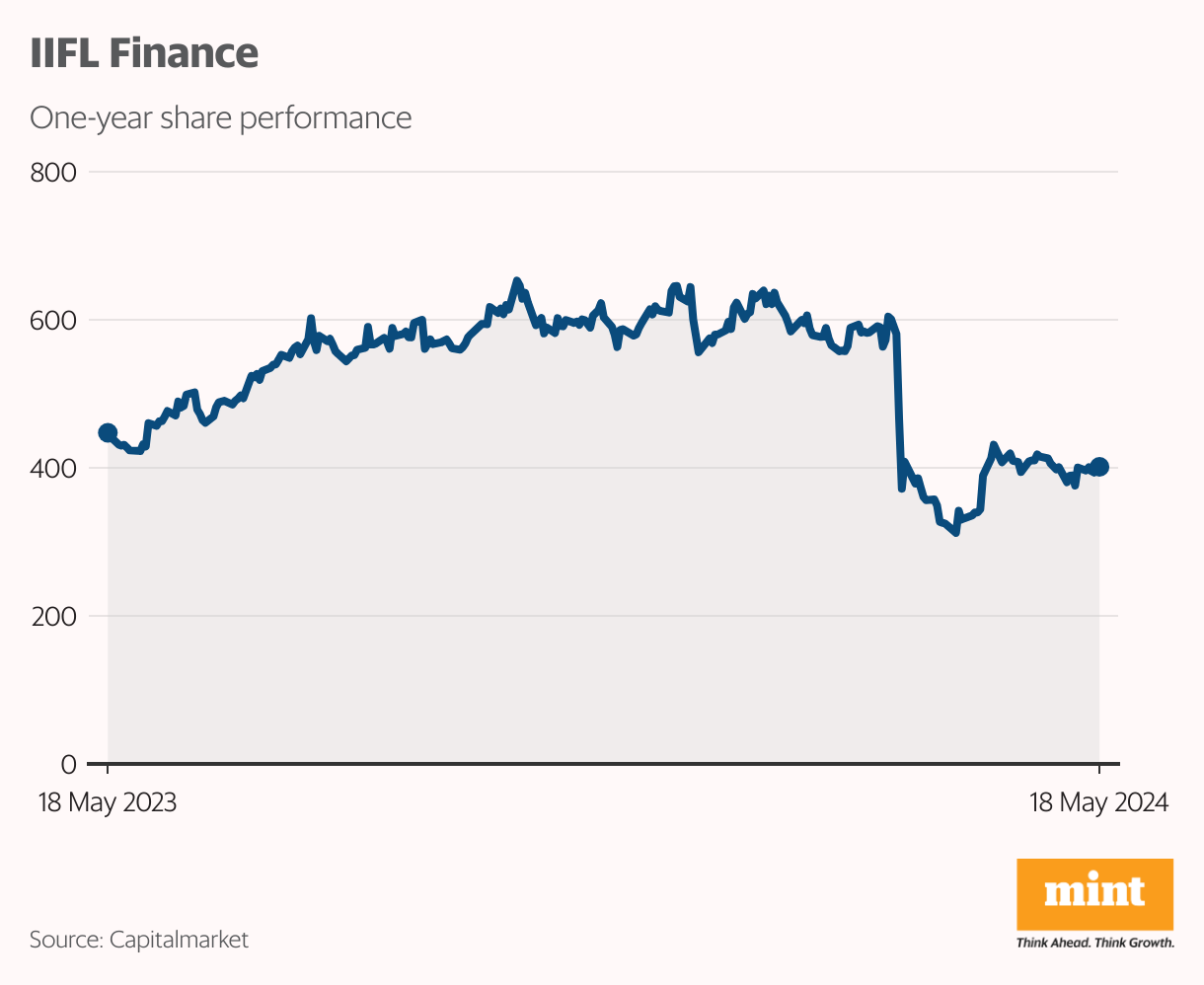

For instance, while looking at the books of non-bank lender IIFL Finance for the financial year ended 2022-23, the RBI found some compliance gaps. In a statement, the regulator said there were “serious deviations” in assaying and certifying purity and net weight of gold at the time of sanction of loans and at the time of auction following a default. It also flagged disbursal and collection of loan amounts in cash, which was far in excess of the statutory limit, among other issues. IIFL was banned from issuing fresh gold loans.

According to a person aware of the development, IIFL was caught off guard, as it had been discussing the issues with the regulator and no official show-cause notice had been issued. The person said that while the violations mentioned by the RBI have been found, such instances are common in the gold loan industry and are not restricted to IIFL.

However, RBI officials contest claims that its directives catch banks and financial services providers off-guard. In many cases, they say, discussions on non-compliance last over a year, giving the lenders time to take corrective action.

Going deeper into the IIFL case, the person cited above said that in conversations with the regulator, the NBFC might have pointed out how giving cash loans beyond the permissible ₹20,000 limit is an industry-wide practice. According to other people in the know, some gold loan companies were using an interpretation of Section 269ST of the Income Tax Act to their benefit. The section prohibits cash transactions of ₹2 lakh or more. Some gold loan companies have used a liberal interpretation of the rule to make cash disbursals of over ₹20,000. This is despite the RBI regulation clearly stipulating ₹20,000 as the cash disbursal limit.

Reports suggest that the regulator has begun cracking down on the practice. Reuters reported on 8 May that the RBI warned some non-bank lenders against disbursing cash loans in excess of ₹20,000.

Experts point out that the RBI has always been a conservative regulator and rightly so, because it has to regulate the business of credit. It has always taken a dim view of any breach of the rules and it is hard to conceive of the regulator condoning violations just because they are prevalent across the industry.

Light Touch Goes Out

The experts also believe that the reason several NBFCs are being schooled is because of the way the central bank looks at non-bank lenders. The regulations governing them are no longer ‘light-touch’ and it wants them—at least the bigger ones—to be as tightly regulated as banks.

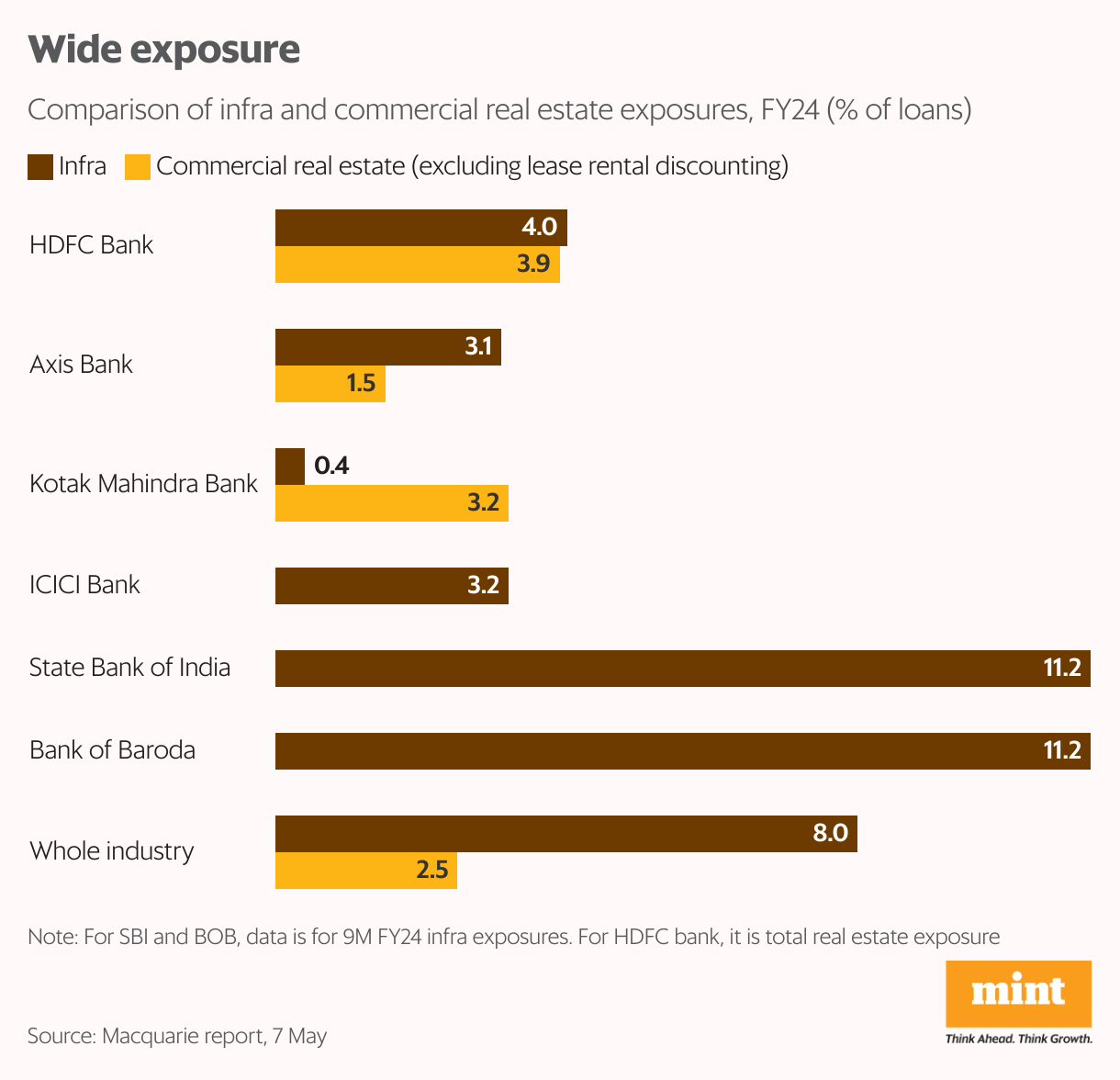

RBI regulations classify NBFCs into four layers based on their size, activity and perceived risks. The upper layer comprises prominent names such as Tata Sons, LIC Housing Finance and Shriram Finance.

“RBI has in various forums, and through regulatory interventions, clearly indicated that the non-banking sector is an important cog in the wheel in the Indian financial sector and complements the banking sector in furthering the goal of financial inclusion,” said Bhavik Hathi, managing director, Alvarez and Marsal.

Hathi said that earlier, the RBI was very focused on banks. NBFCs were treated as ‘shadow banks’ globally and in India. “This view has changed and global regulators as well as the RBI are now treating them as an important link in the ecosystem, along with payment companies and other fintechs,” said Hathi.

Beyond Moral Suasion

While there have been some broad changes at the supervision level since Das took over, such as the consolidation of departments supervising commercial banks, non-bank lenders and urban cooperative banks so that they do not work in silos, the RBI’s enforcement actions have actually evolved over time.

What used to be a gentle nudge till the 1990s became a stronger prod in later years. According to R. Gandhi, a former RBI deputy governor, the RBI used moral suasion as a tool for enforcement, giving banks hints to course-correct. Then came the infamous securities market scam of 1992 involving Harshad Mehta and some banks.

“This was the first time penalties were imposed on some banks,” said Gandhi, who was a deputy governor at the central bank for three years, till April 2017. “At that time, in the 1990s and 2000s, when the RBI penalised a bank, it was seen as a hit to the lender’s reputation and got the desired result.”

In 2013, a couple of decades later, the Financial Sector Legislative Reforms Commission (FSLRC), set up by the government in 2011 and led by former justice B.N. Srikrishna, released its recommendations, leading to the formation of a new wing at the RBI.

“The commission said that all regulators should have an enforcement wing, independent of regulation and supervision. The RBI’s enforcement department was set up in 2016. This meant that the regulator should frame the rules, supervisors should check if those were being followed, and the enforcement wing should take action if rules are broken,” said Gandhi.

Prior to this, the supervisors were investigating regulated institutions and penalising them as well, when wrongdoing was found. Since the change, any transgression recorded by the supervisory wing is transferred to the enforcement wing, which takes action after seeking an explanation for the lack of compliance.

Gandhi explained that after the new department was set up and there was a more focused effort by the RBI, the frequency of such enforcement actions has been rising. However, as time progressed, these penalties seemed paltry in comparison to how big banks had grown. They were also not getting the desired results.

At the same time, digital banking has made greater inroads and a regulatory violation is no longer restricted to a transaction or a branch or a region; it is institution-wide. Hence the correction needs to be across, said Gandhi, adding that it means the existing way of conducting business needs to change completely.

“The RBI has to look for some way that the entire sector takes notice. When business restrictions are imposed, the entire management and the board get into action as their profitability is at risk,” said Gandhi.

In private conversations, leading lenders have two very different things to say about the RBI’s approach to supervision and regulation. Some said the RBI’s strictures have helped them understand the flaws in the way they do business and it is because of these stringent measures that India has not seen the kind of bank failures other countries have witnessed. Others decried the actions, saying that the regulator was way too harsh.

Appellate Tribunal?

Given the rising instances of actions by the RBI, there is a growing chorus within the industry on the need for an appellate tribunal, where these enforcement orders can be challenged. Kotak Mahindra Bank took the RBI to court in 2018 appealing against the regulator’s decision on the route Uday Kotak took to reduce the promoter stake. The bank withdrew the case after a settlement that allowed the promoter to reduce the stake to 26% in six months. This, however, did not embolden others.

“Notably absent is an appellate authority specifically designated for challenges to decisions made by the RBI. As it stands, decisions made by the RBI are considered final and can only be contested in the high courts or higher civil courts,” said Debashree Dutta, founder and partner of Vritti Law Partners.

Dutta believes there is definitely a need for an appellate tribunal for RBI diktats. “Maybe the government should reconsider the recommendations of the Financial Sector Legislative Reforms Commission for a financial sector appellate tribunal for all the regulators, including the RBI.”

- Top Gainers

- Top Losers

- 52 Week High